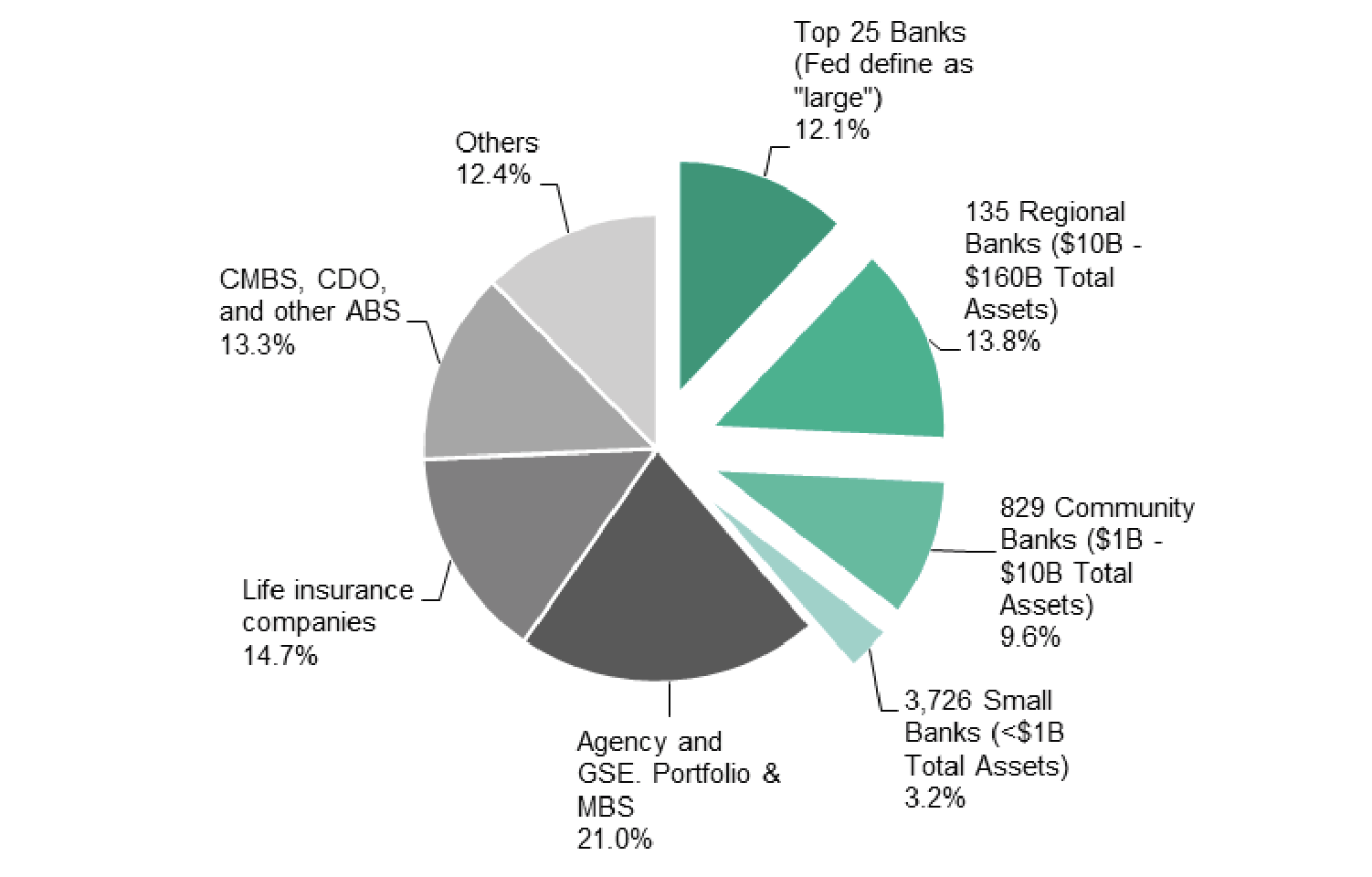

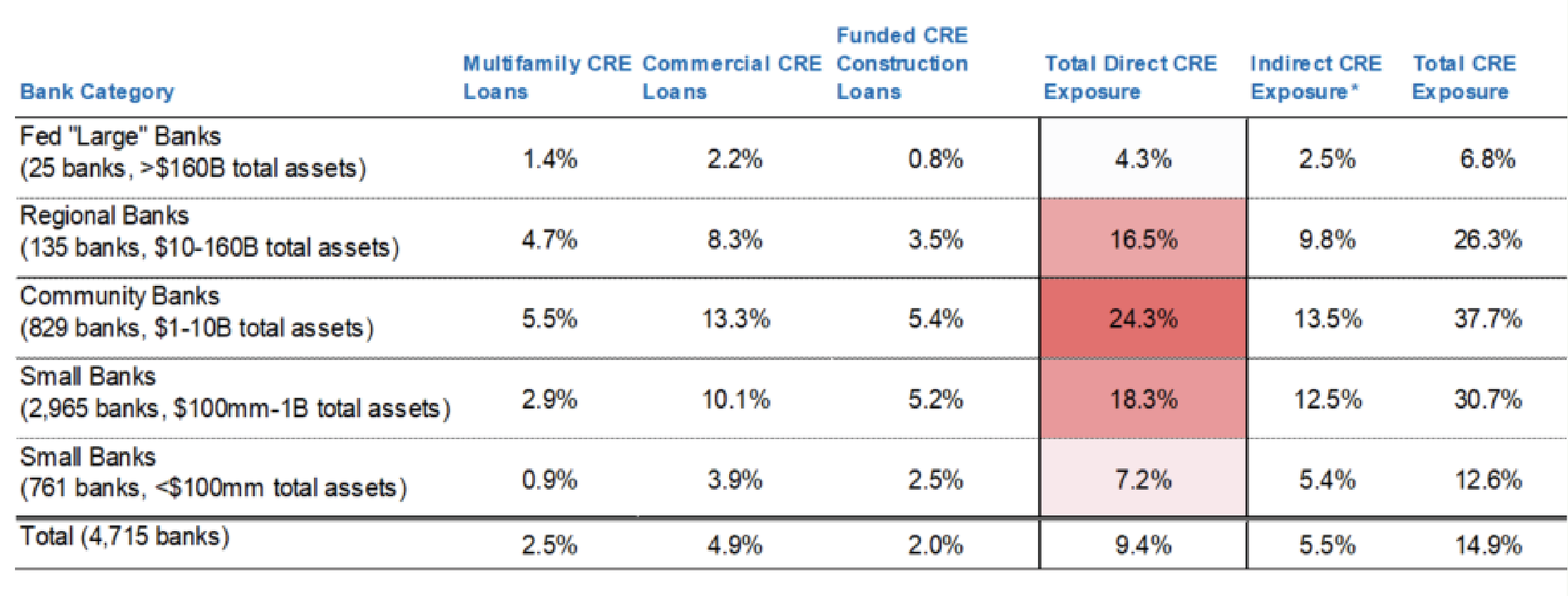

We aim to quantify banks’ exposure to CRE and assess the potential for realized loan losses.

While the average share of CRE loans as a percentage of total assets at regional and community banks suggests manageable exposures, there is wide distribution around that average.

For instance, 33% of regional banks and 44% of community banks have CRE loan exposure at 25%-50% of total assets.

Given that these banks are levered at roughly 8x-10x equity, significant write-downs of CRE loans could substantially reduce these banks’ equity positions.

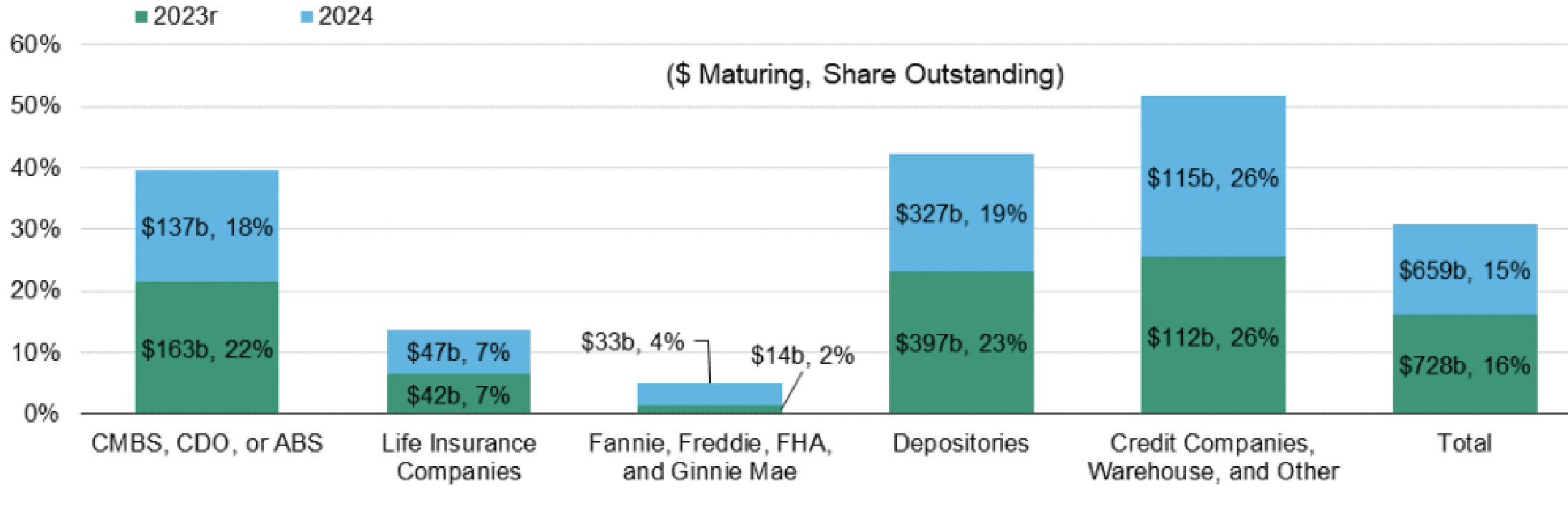

Most of the near-term maturing debt was originated in the 2013 through 2018 timeframe. Given the significant rise in interest rates since then, analysts are worried that properties in troubled sectors (predominantly office and some areas of retail) may not be able to refinance maturing debt without significant additional sponsor equity contributions and may therefore default.

According to Green Street Advisors, property prices across CRE have declined by 15% from 2022 peaks with office experiencing the largest decline at 25%. Green Street bases its commercial property index on transaction prices vs. appraisal data.

The NCREIF Index was down 3.5% in Q4 2022, the first meaningful quarterly decline since 2009. The NCREIF index is based upon appraisal data which tends to be lagging and less volatile than transaction-based data.

Real estate professionals expect the NCREIF Index to decline 5.3% in 2023 but rise 4.5% in 2024 and 6.4% in 2025. Office is expected to be the worst performing asset class in 2023 at -9.1% followed by industrial and apartments at -5.1% each.

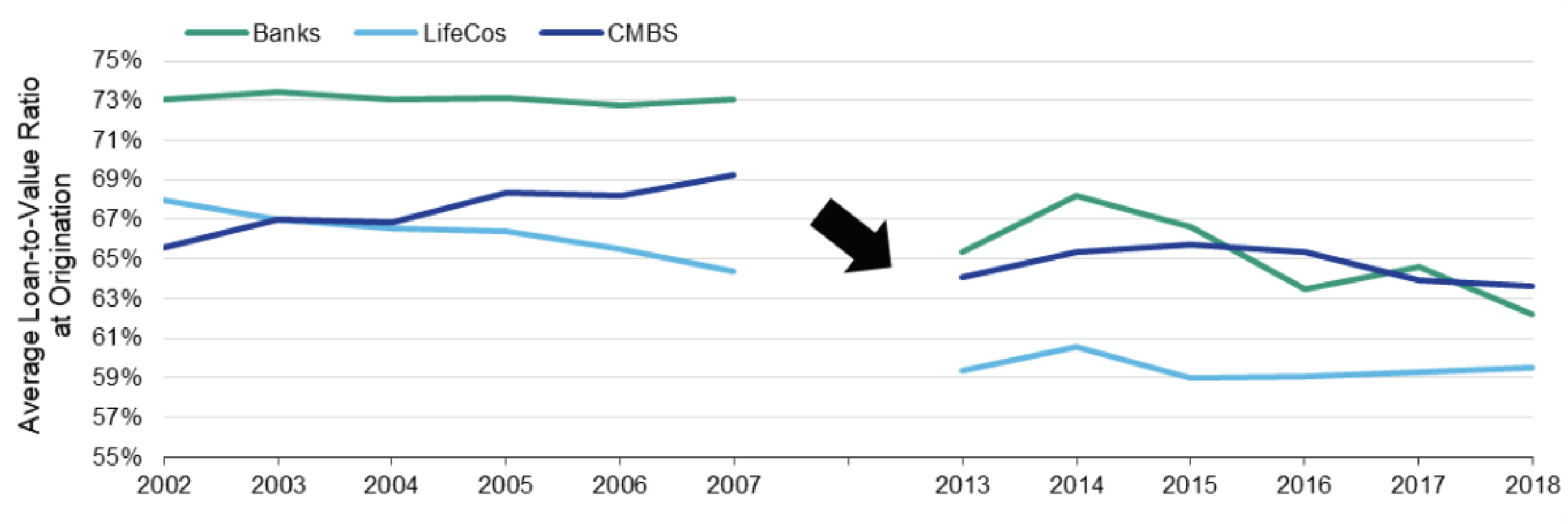

Loans were originated at lower LTVs (on average 5%-10% lower than those originated prior to the GFC).

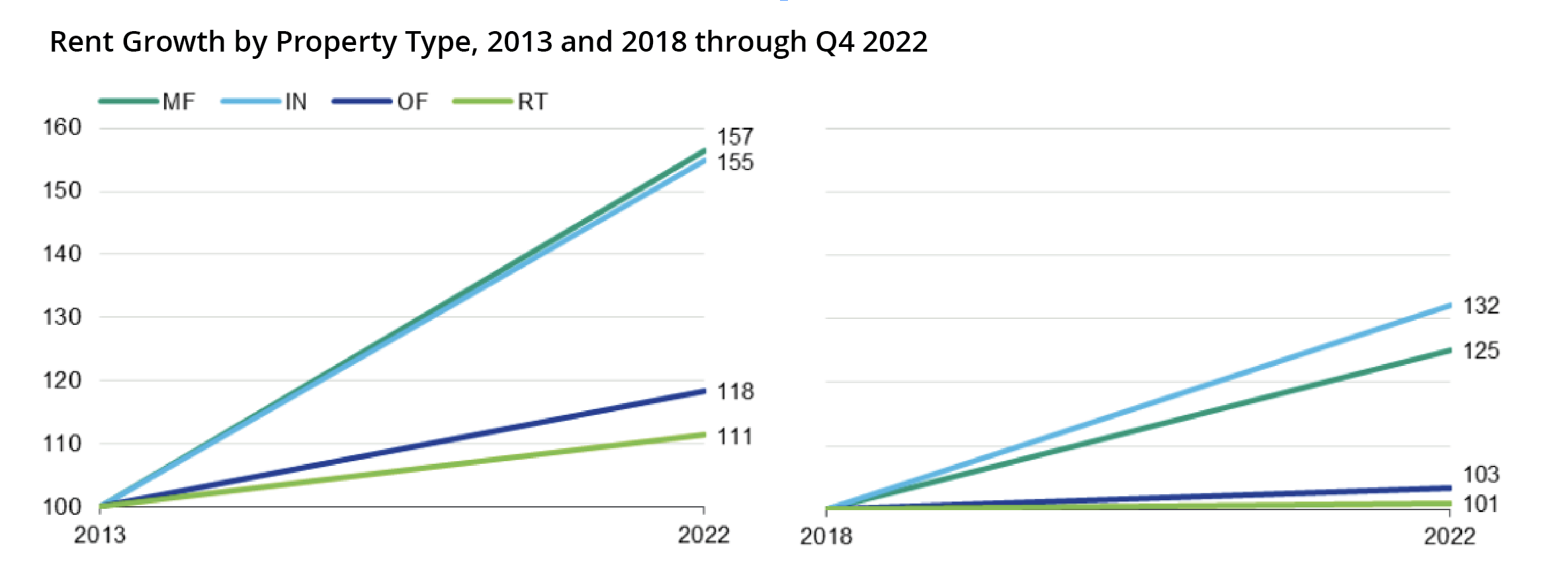

Most CRE has benefitted from strong rent growth over the past several years (especially for multi-family and industrial properties). This should support higher values upon loan refinance in 2023 and 2024 despite increased cap-rates.

Q1 2023 saw strong US employment and economic data, which led to a spike in US Treasury yields. The collapse of Silicon Valley Bank and Signature Bank on March 10th

The seven-year forecast predicts mid-to-high single digit equity returns, mid-single digit returns for US government debt and investment grade bonds, and higher returns for new private market strategies. The forecast

Inflation data in the US has been mixed in 2023, with headline CPI declining on a YoY basis but core CPI remaining high. While leading indicators suggest decelerating inflation rates,

US economic growth is expected to decelerate, with the risk of a mild recession in H2 2023 or early 2024. A severe credit crunch could occur if lending is significantly

The trajectory of equity markets will be determined by interest rates, economic growth, outlook for corporate earnings, and potential for large sustained financial system disruptions. There are three potential scenarios

Equity markets have appreciated YTD across all major regions, with growth stocks outperforming value stocks. Valuations are generally fairly valued to modestly overvalued relative to historical averages, but confidence in

We discuss the performance and valuation of safe fixed income investments. Yields have pulled back since March due to concerns about US regional banks, and while signs of stress are

The HFRX Hedge Fund Index was flat in Q1 2023, with convertible arbitrage and credit strategies performing best while global macro/trend following strategies performed worst. Private real estate showed mixed

We highlight actionable investment opportunities across various asset classes, including short-term US and Canadian government debt, high-yield bonds, private credit strategies, preferred and structured equity, venture debt, and new allocations

BCA is not for everyone – and we are proud of that distinction. We look for a select group of individuals (and their entities) whose financial position and preferences enable them to thrive while working with us.

We welcome your interest. Please give us at call at +1-406-556-8202 to set up a confidential exploratory consultation.