We consider the following factors when developing our 7-year forecasts.

The era of ultra-low interest rates is likely over with interest rates remaining elevated for longer.

Labor shortages persist in service-oriented industries and may constrain margin expansion.

Energy prices are likely to be higher vs. the prior cycle given structural supply shortages.

Geopolitical uncertainty is increasing with regards to the US-China relationship and potential for episodic military conflicts.

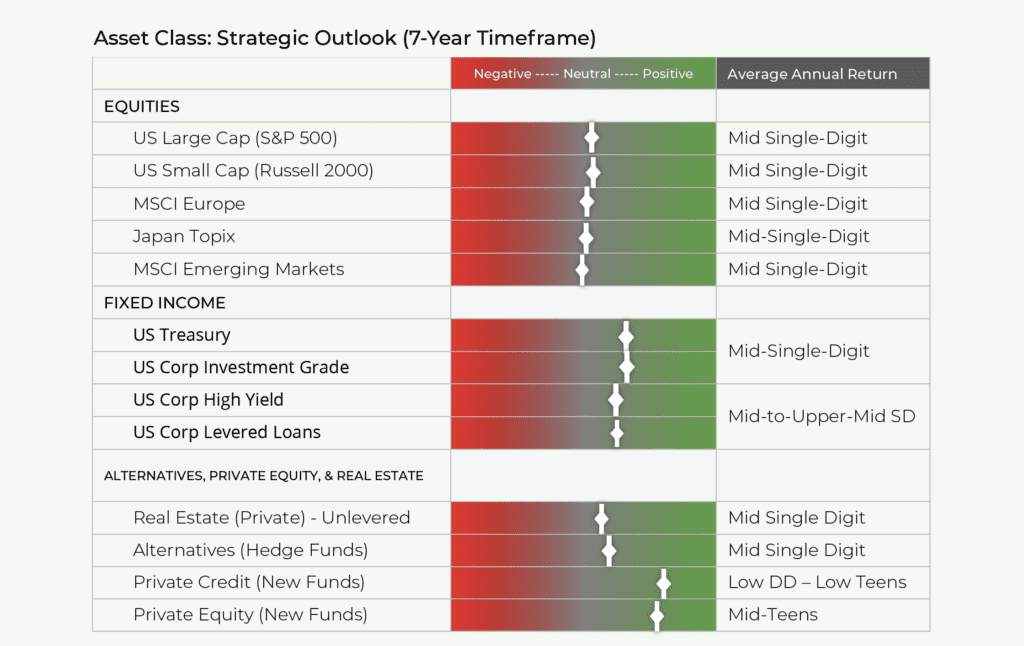

With equity valuations having declined significantly in 2022, we now expect mid-to-high single digit nominal pre-tax annual equity returns (6.5%-7.5%) over a seven-year forecast period.

We continue to expect greater convergence between US and International equity market returns. While we expect quality and growth stocks to outperform value stocks over the forecast period, the rate of outperformance is likely to be lower than in recent years. We still anticipate significant volatility over the next 6-12 months as interest rates are yet to peak and many economic indicators appear to be slowing rapidly. However, inflation clearly seems to be in retreat and China’s reopening should lend support to global growth.

The effects of the recent US bank failures and potential wider spillover to US regional banks remain to be seen. A swift pullback in bank lending would result in credit contraction and likely lead to a faster and potentially more severe recession (although this is not our base case).

“Safe” fixed income remains attractive, especially for shorter-term maturities

US and Canadian 1-year Treasury bond yields are still yielding 4.4% to 4.6% while shorter-term (6 month) yields are even higher at 4.6% to 4.9%. However, mid-term (7-to10-year maturities) bond yields have dropped swiftly over the past month and now only yield 2.8% to 3.4%.

We still expect mid-single digit returns for US government debt and investment grade bonds over the forecast period.

On a risk-adjusted pre-tax basis, safe fixed income is still quite attractive relative to equities.

Riskier credit assets (high-yield bonds and leveraged loans) are also attractive over a mid-term time frame (and on a relative basis to equities)

US high-yield bonds are now yielding 8.2% with 7-year forecasted annual returns of 7.0% (inline with US equities). Leveraged loans are currently yielding 10.1% (based on 3-year takeout convention) with expected mid-term annualized returns in the 7.0% range.

However, on a nearer-term basis (next 12 months), high yield bonds and leveraged loans may experience declines and heightened volatility if credit spreads widen further were a deeper than expected recession to occur.

For new private market strategies (i.e., private equity, private credit, real asset funds), we continue to forecast higher returns relative to public markets (over a multi-year timeframe).