After a sharp rally to start the year, the trajectory of equity markets will be determined by a) path of interest rates, b) economic growth and outlook for corporate earnings and c) potential for large sustained financial system disruptions or “accidents”.

For the first time since late 2021, risks regarding inflation vs. economic growth appear two-sided.

It is clear that the Fed is close to ending its rate hike campaign. What is not clear is when the Fed begins cutting rates. Across previous rate hike cycles, the Fed has typically cut rates shortly after the last rate hike. Historically, these rate cuts have generally been large in magnitude and swiftly implemented over a six-to-twelve-month period.

However, elevated inflation levels are a key difference between this cycle and prior cycles.

On the one hand, a pause in interest rate hikes followed by rate cuts is clearly positive for equity markets. However, investors appear too optimistic regarding rate cuts and not pessimistic enough regarding the potential for recession and the resultant decline in corporate earnings.

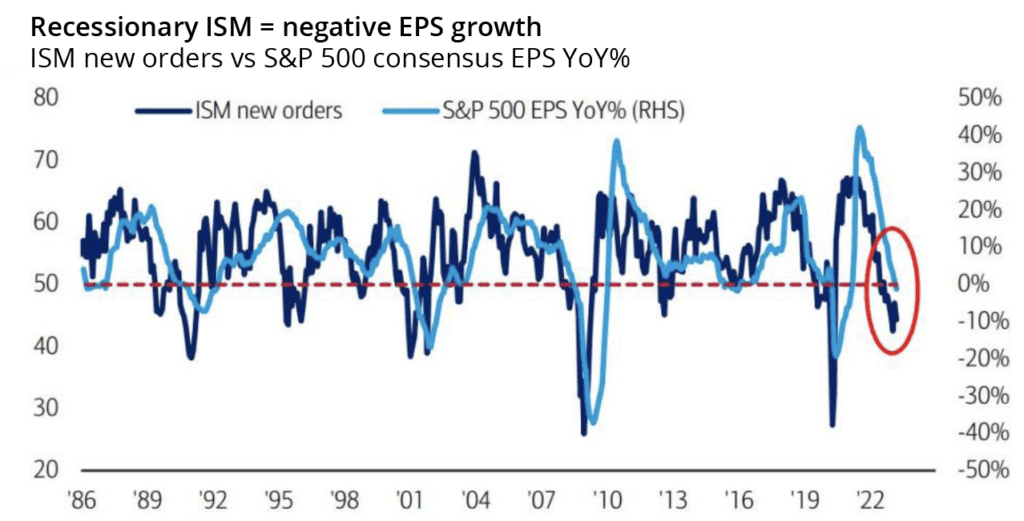

US and European manufacturing indexes have been below 50 (indicating contraction) for several months and new orders are declining at faster rates.

As seen in the chart below, historically, when the ISM new orders declines into the mid-40s , earnings have tended to decline between 10%-20% (higher in the GFC).

In the first couple of weeks post-SVB, commercial and industrial loan issuance declined significantly before stabilizing over the past few weeks. If credit curtailment to small-and-mid-sized businesses intensifies, there will likely be ripple effects felt throughout the economy.

Tougher credit availability coupled with dimmer views on sales and expansion plans has helped drive the NIFB’s small-business optimism index down to its lowest levels in three months and well below pre-pandemic levels.

Thus far, corporate earnings have largely been resilient as end demand has remained reasonably strong across many sectors. In 2022, S&P 500 companies experienced modest margin compression (especially in Q4 2022). Given top-line revenue strength, S&P earnings still expanded by 5% for the full year but declined by 3% YOY in Q4 2022.

Analysts expect 2023 S&P 500 earnings to be relatively flat vs. 2022 with YOY declines in H1 followed by YOY gains in H2.

We believe that these projections remain optimistic as the economy has yet to feel sustained effects on demand from the Fed’s 2022 interest rate hikes.

In 2023 and 2024, the unknown is to what degree corporate earnings fall. In prior recessions, earnings have declined between 10% to 30% from peak to trough.

In prior downturns, equity markets typically did not trough until forward earnings estimates stopped declining.

While S&P 500 forward earnings estimates have declined modestly from $240 to $225, should a deeper-than-expected recession emerge, these forward estimates would need to be revised downward substantially.

As seen in the collapses of SVB and Signature Bank, sharp increases in interest rates can have unexpected and unintended consequences that emerge seemingly out of the blue. Risks for financial market instability or accidents have certainly increased in recent months.

The sharpest and swiftest equity market downturns typically occur when these accidents do happen with fears of financial instability and lack of liquidity becoming widespread.

We continue to see multiple potential paths for equity returns over the next 6-12 months (with reference to the S&P 500 which stands at 4,138 as of April 14, 2023).

Scenario A: (Optimistic Case) – Inflation moderates much faster than expected with a soft landing and a mild earnings recession. Fed pauses rate hikes by May and cuts rates by year-end 2023.

Under this scenario, we see goods inflation reaching firmly negative territory and services inflation starting to decelerate. The S&P 500 displays earnings resiliency and investors price in that 2023 earnings represent trough earnings (with ~5% S&P 500 earnings declines vs. 2022) and look forward to resumption of earnings growth in 2024 with interest rates remaining stable / gradually declining. Equity markets may decline moderately (5% or so) from present levels before rallying to end 2023 in the 4,200-4,500 range.

Investors are already pricing in a decent probability of this case occurring.

Scenario B: (Base Case) – Moderating inflation and rate hikes in line with Fed expectations coupled with a modest corporate earnings recession.

Under this scenario, goods inflation declines or moves to deflation while services and shelter inflation remain higher than desired.

The Fed hikes once or twice more with a terminal Fed Funds rate slightly north of 5%. However, the Fed then keeps rates at this level for the next 9-12 months. The US economy enters a moderate recession with 2023 S&P 500 corporate earnings down 10%-15% vs. 2022.

Under this scenario, the S&P 500 could likely decline 10%-15% from present levels. We expect markets to remain relatively range bound with periodic bouts of rallies and sell-offs as the ultimate path of rate hikes remains unclear. In this scenario, the market may end 2023 in the 3,800-4,200 range.

Given that the S&P 500 is presently at 4,138, investors have assigned the highest probability of this case occurring.

Scenario C: (Pessimistic Case) – Core inflation remains higher for longer leading central banks to maintain peak rates for longer. The economy slows faster than expected followed by a financial market crisis which leads to severe global recession. This scenario leads to faster and deeper equity market declines followed by a sharp rebound once Fed policy pivots.

Under this scenario, investors begin to reprice Fed Funds terminal rates north of 5%. The chances of a global shock and severe recession increases. Under this scenario, S&P 500 earnings may decline 15%-20% and equity markets may decline by 20%+ from current levels over the next 6-9 months.

However, such events also increase the chance for an ultimate swift Fed pivot with declining interest rates which would ultimately lead to sharp equity rallies. It is very conceivable under this scenario for the S&P 500 to fall to 3,200-3,500 level over the next 6-9 months.

At this stage, outcomes remain highly uncertain and may be influenced by a large number of external variables that are difficult to predict.

With regards to legging into equities, for investors with a mid-term (5-year+ framework), we would continue looking to begin adding to equities around the 3,600-3,700 S&P 500 level while becoming more constructive at the 3,300 range.