Performance

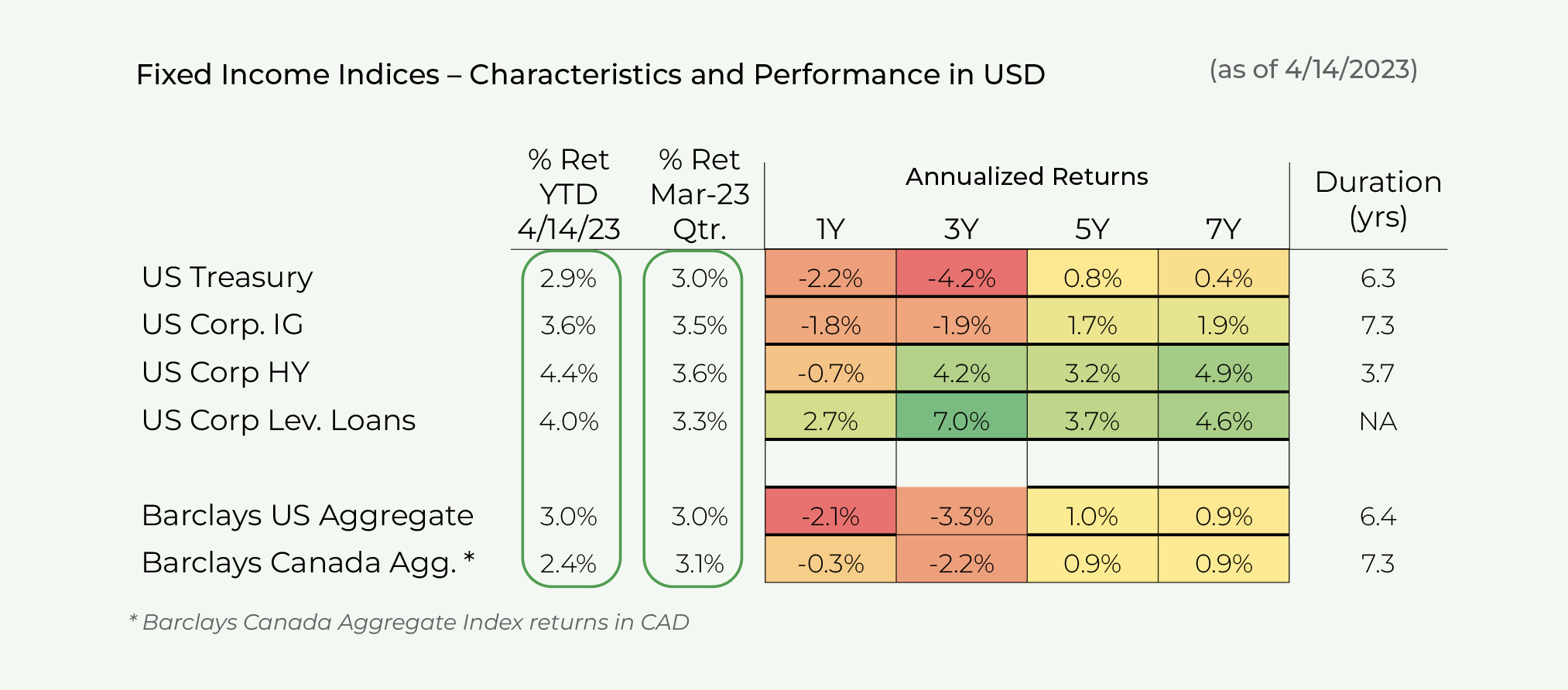

Safe fixed income (government bonds and corporate investment grade bonds) appreciated sharply YTD as interest rates swiftly declined during March.

After interest rates peaked in early March following surprisingly robust US January employment figures and higher than expected inflation, rates swiftly declined throughout March following the collapse of SVB and Signature Bank on March 10th. These banking collapses triggered broader concerns surrounding the stability of US regional banks and the potential for pullbacks in credit and lending.

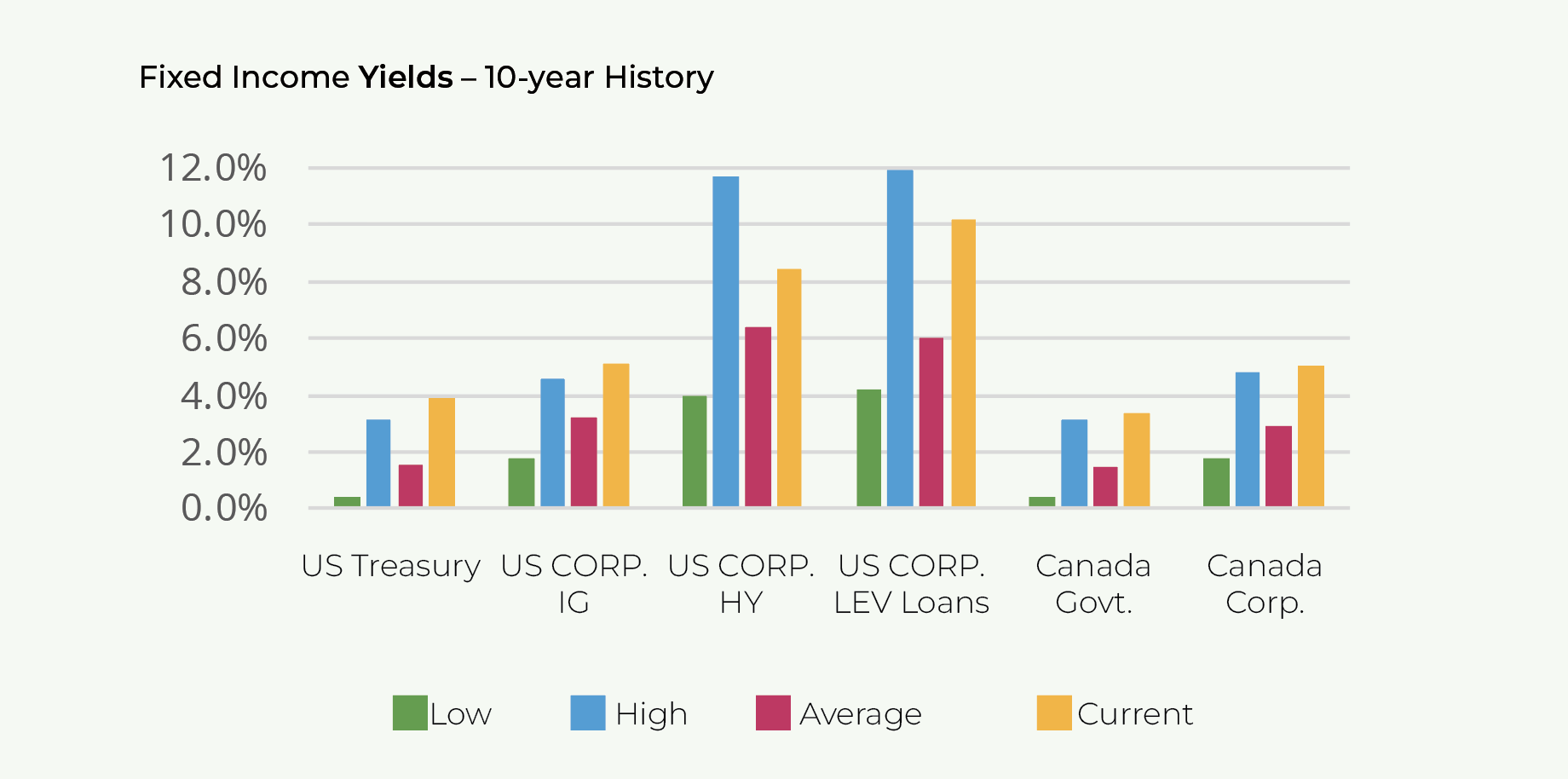

2-Year Treasury yields pulled back from 5.1% to 4.2% presently and 10-years yields have pulled back from 4.1% to 3.5% as of 4/14.

Additionally, inflation data for March was generally inline or lower than expectations with a sharp slowdown in YOY wage growth and pullbacks in terms of producer prices paid.

Both high yield bonds and leveraged loans have appreciated YTD.

HY bonds primarily benefitted from the decline in Treasury base rates while leveraged loans benefitted from high current income and modest price appreciation from tightening spreads.

Valuation

Safe fixed income (government bonds and investment grade corporate bonds) yields remain at attractive levels but have pulled back meaningfully from early March highs.

US Treasuries are yielding roughly 4.0%-4.6% for 1-to-2-year maturities and 3.6% for 10-year maturities.

US corporate investment grade bonds are now yielding 5.0% (with risk of default very low).

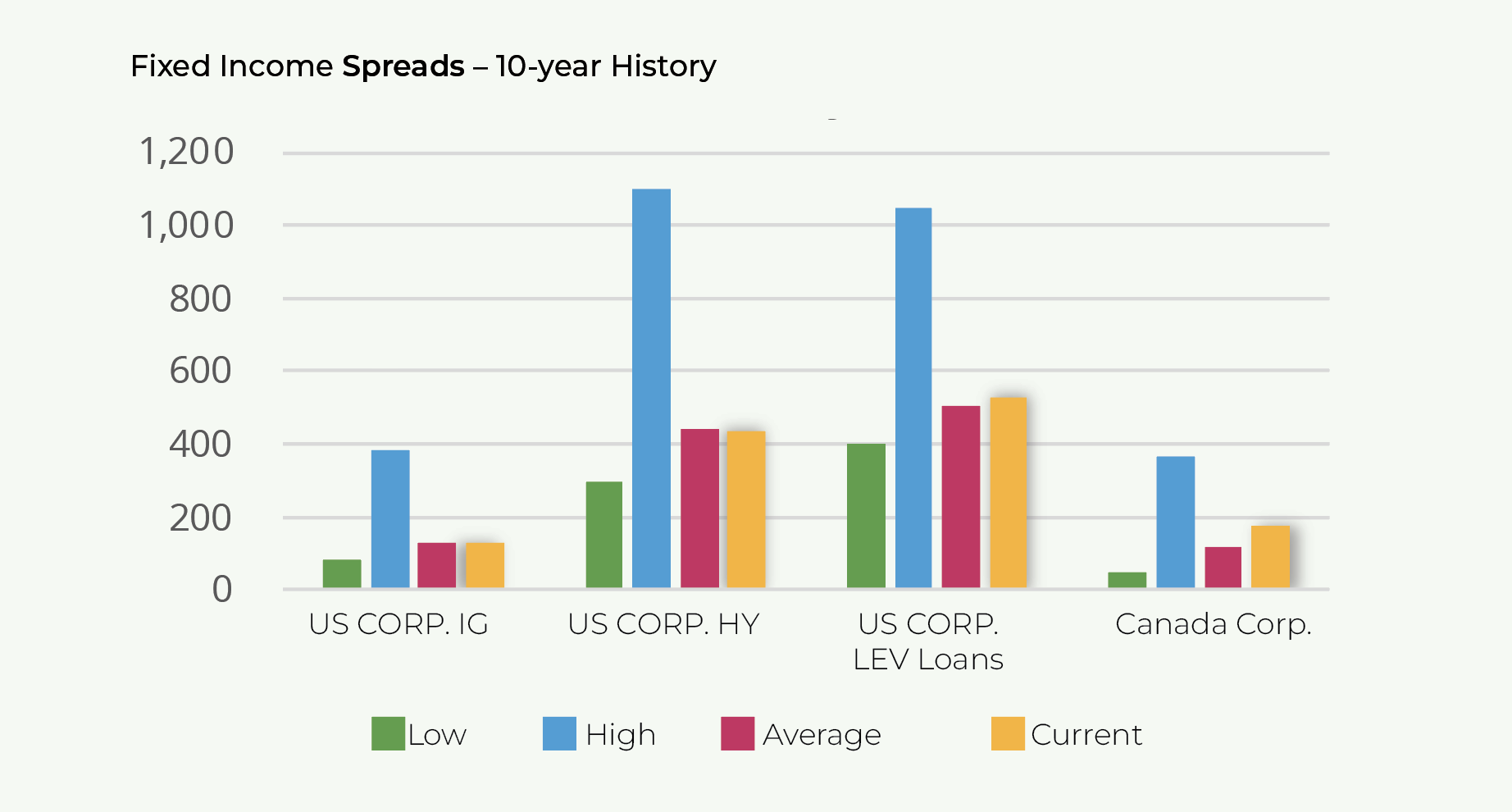

Corporate spreads (investment grade and high yield) have remained relatively flat YTD.

IG spreads are presently at 132bps and HY spreads are at 440bps (inline with longer-term averages).

Spreads have generally widened further during recessionary periods (200bps for corporate bonds and 800bps for HY bonds).

However, the quality of the high yield index is much stronger now than in previous periods. When coupled with today’s high base rates, it is unlikely that spreads will widen to those experienced in previous recessions (even if economic activity slows substantially).

Credit performance remains generally strong with default rates well below historical levels. However, signs of stress are starting to emerge with default rates and bankruptcy filings increasing (off very low base levels).

Defaults are likely to increase in 2023 and 2024 as economic growth slows, corporate earnings decline, and companies with weak balance sheets or nearer-term refinancing obligations face capital raising challenges. We expect that the default severity will be much lower than that experienced during the GFC.