Performance

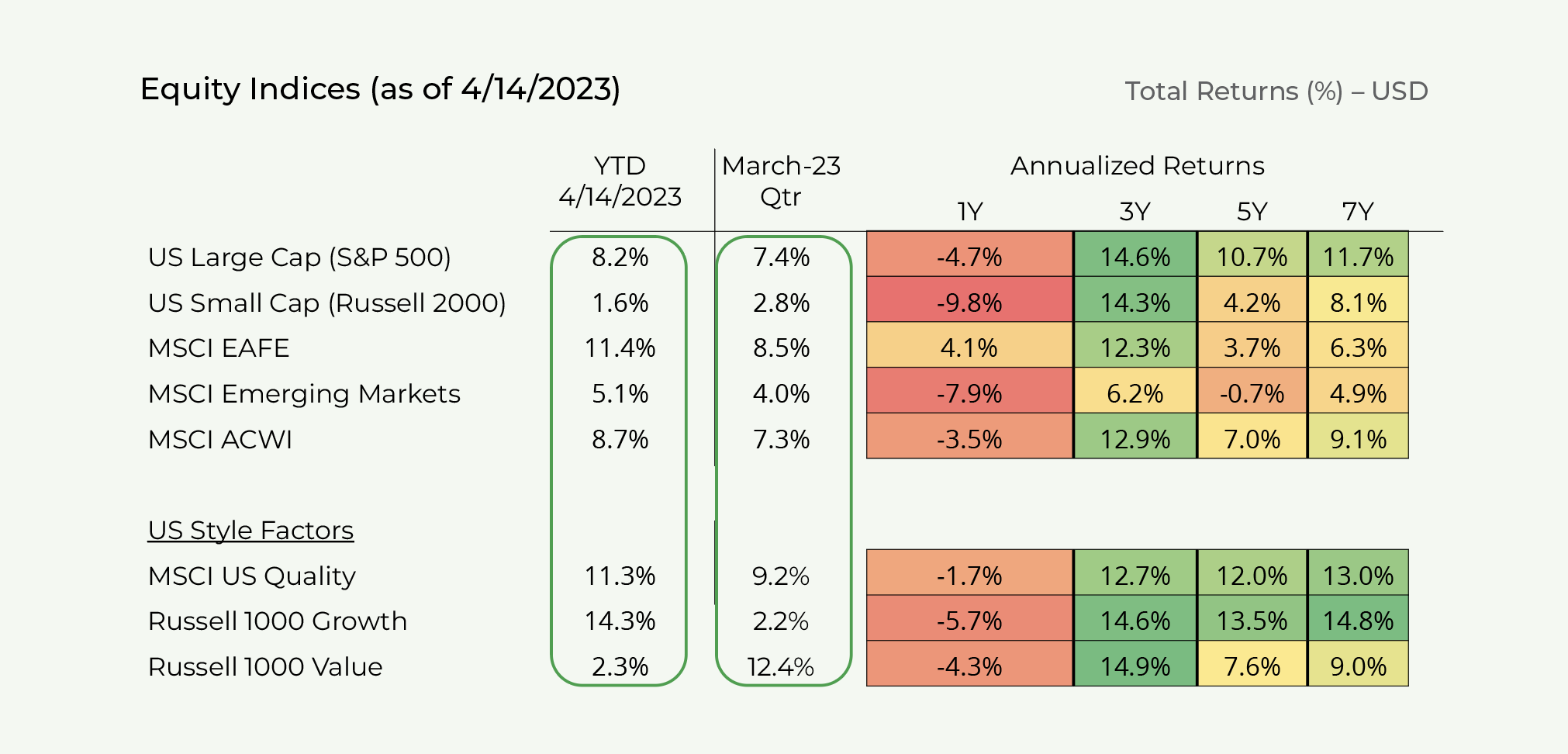

Equity markets (MSCI ACWI Index) appreciated by 8.7% YTD through April 14th.

Equity market gains have been broad-based across all major regions with international developed markets (primarily Europe) demonstrating the largest gains at +11.5% YTD in USD through April 14th.

Growth stocks (+14.5%) materially outperformed value stocks YTD (+3.3%) as US interest rates declined swiftly in March.

Technology, consumer discretionary, and communication services (largely internet) stocks outperformed YTD.

Energy, industrials and materials sectors significantly outperformed during Q4 (up 16.0%-17.7%) while consumer discretionary, communication services, and technology sectors underperformed (down 0.5% to +5.2%).

US large-cap equities (S&P 500) are up 8.1% YTD and 16.2% since October 2022 trough levels.

The YTD rally has been very narrow, led by a few large cap technology, consumer discretionary and internet companies.

The average stock in the S&P 500 is only up 3% YTD. As such, the index may retreat significantly if some of these large cap companies were to experience share price declines post Q1 earnings.

US small-cap equities (Russell 2000) have underperformed and are only up 1.7% YTD.

Small caps have been hit hard by greater weakness among financial companies (15% of index weight) and by increased recessionary fears as investors believe that small caps are more susceptible to demand reductions and wage pressures.

European equities are up 11% YTD and have rallied 23% from September 2022 trough levels.

Thus far, macroeconomic conditions have held up much better than expected in Europe (warm winter and generous government subsidies). Additionally, European exporters and luxury goods companies have benefitted from China’s reopening.

However, macro conditions may become more difficult as the impact from the ECB’s rapid rate hikes is yet to be fully felt by businesses and consumers. Additionally, core inflation remains at peak levels which may lead to the ECB maintaining higher interest rates for longer relative to other regions.

Chinese equities are up 12% YTD and have rallied 34% from September 2022 trough levels.

While the easy money has been made already, we still expect that Chinese equities may outperform over the next 12 months as China continues to benefit from increased domestic consumption post COVID reopening, increased governmental stimulus (as the government aims to meet its 5% real GDP growth targets), and a more constructive regulatory posture especially with regards to large-cap internet and e-commerce companies.

Q1 corporate earnings season kicks off in earnest over the next few weeks. 2023 guidance will be heavily scrutinized in terms of a) revenue growth assumptions and demand outlooks and b) margins – input and labor cost outlooks.

Thus far, the big banks reported very robust earnings and their stock prices appreciated following results.

Regional banks quarterly reports will be highly scrutinized. Investors will assess banks’ deposit trends (what level of outflows were experienced post SVB collapse), the level of unrealized bond losses, changes in provisions for loan losses, and commentary regarding the lending environment and any potential tightening of credit or pullback in lending.

Large-cap technology and internet companies may face a challenging earnings season. These stocks have rallied substantially with the NASDAQ up 20% YTD.

These gains have been driven by a combination of falling interest rates and investor rotation away from bank and other cyclical stocks as recession fears have mounted.

However, valuations for mega-cap technology and internet stocks have risen and the shares are susceptible to pullbacks from any earnings disappointments. Fundamentals in the sector could weaken if macroeconomic pressures intensify.

For investors with a mid-term time frame, we continue to believe that stocks of high-quality companies will outperform given their strong business models, superior earnings growth and strong returns on capital.

YTD, quality and growth stocks have materially outperformed value stocks. However, value stocks may outperform post Q1 earnings season if a) interest rates rise again or b) earnings reports for large-cap quality and growth stocks disappoint lofty expectations.

Valuation

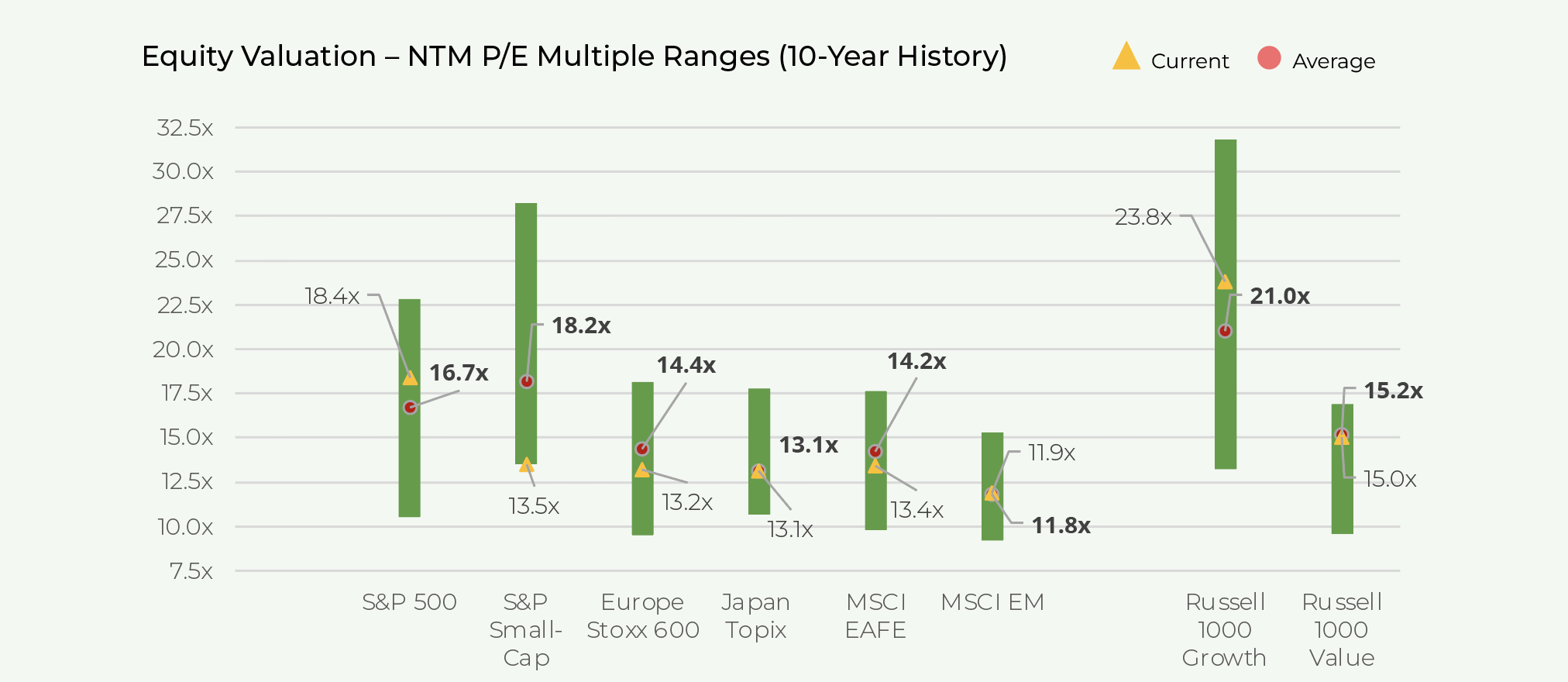

Equity markets are generally fairly valued to modestly overvalued relative to historical averages.

The S&P 500’s forward P/E multiple has compressed from 21.5x at the beginning of 2022 to 18.4x today (modestly above historical averages).

International developed markets are trading at 13.4x forward earnings (roughly 7% below historical averages) while emerging markets are trading at 11.9x forward earnings (inline with historical averages).

However, confidence in forward earnings is much lower than normal given the backdrop of still high interest rates and inflation, China reopening, geopolitical tensions, and higher potential for recession in the US and Europe.

Equity market valuations are no longer cheap compared to bonds.

The S&P 500 presently trades at 18.4x consensus NTM earnings (which may be too high).

Historically, the S&P 500 earnings yield (inverse of multiple) has averaged 200-300bps over 10-Year Treasuries. Based on that metric, a 15x-18x forward EPS multiple is “fair” for the S&P 500.

Additionally, our mid-term return outlook for credit (high yield bonds and leveraged loans) is similar to that for equities, with lower risk.