We consider the following factors when developing our 7-year forecasts.

Interest rates are likely to decline from current levels but will remain at higher levels for longer versus the past ten-year average.

Labor shortages persist in service-oriented industries and may constrain margin expansion.

Energy prices are likely to be higher versus the prior cycle given structural supply shortages.

Geopolitical uncertainty is increasing with regards to the US-China relationship and potential for episodic military conflicts.

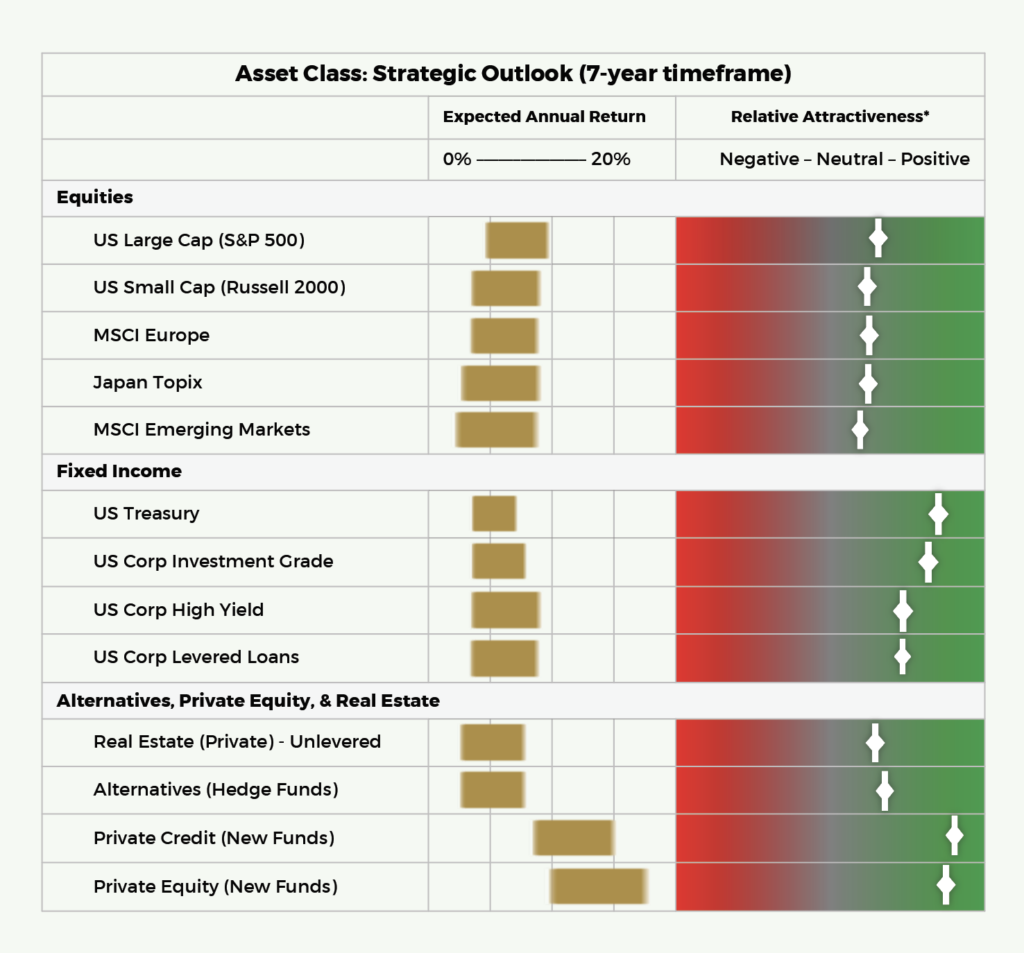

With equity valuations having increased YTD but having eased in Q3, we expect mid-to-high single digit nominal pre-tax annual equity returns (6.5%-8.0%) over a seven-year forecast period.

We anticipate greater convergence between US and International equity market returns.

While we expect quality and growth stocks to outperform value stocks over the forecast period, the rate of outperformance is likely to be lower than that over the past seven years.

Equity market valuations are generally fair (for international markets) to modestly overvalued (US).

As such, expected returns are likely driven by earnings growth and dividends rather than multiple expansion.

Potential wildcards (especially for tech-oriented US markets) include adoption pace surrounding generative AI and the resultant potential for above-trend revenue growth and margin expansion.

“Safe” fixed income is highly attractive, with compelling shorter-term and mid-term maturities.

US and Canadian 1-year government bond yields are yielding 5.3% to 5.4% and 2-year government bonds are yielding 4.9%-5.1% (as of 10/10/23).

US 10-Year Treasuries are yielding 4.6%. These yields are highly compelling as we believe the Fed rate hike cycle is close to over and inflation is subsiding. If 10-year yields were to decline to a 3.5% level (which we think is reasonable if either inflation subsides faster than expected or if a recession ensues), the capital appreciation potential for these bonds is strong.

We expect mid-single digit returns for US government debt and investment grade bonds over the forecast period.

On a risk-adjusted pre-tax basis, safe fixed income’s return potential is very compelling relative to equities.

Riskier credit assets (high-yield bonds and leveraged loans) are also reasonably attractive over a mid-term time frame (and on a relative basis to equities).

US high-yield bonds are now yielding 9.0% with 7-year forecasted annual returns of 7.5% (relatively close to US Equities). Leveraged loans are currently yielding 10.2% (based on 3-year takeout convention) with expected mid-term annualized returns in the 7.0% range.

These high yields are primarily due to high base rates. Spreads remain near historical averages and could easily widen in a recession.

For new private market strategies (i.e., private equity and private credit,) we continue to forecast higher returns relative to public markets (over a multi-year timeframe).

* The attractiveness of each asset class (as depicted by the positioning of the sliders) is based upon risk-adjusted returns when considering expected returns, volatility, and liquidity. Thus, US Treasuries with mid-single digit returns are shown as highly attractive given a low-risk profile whereas public equities are only rated modestly attractive despite their higher expected return as equities have much greater volatility.