Performance

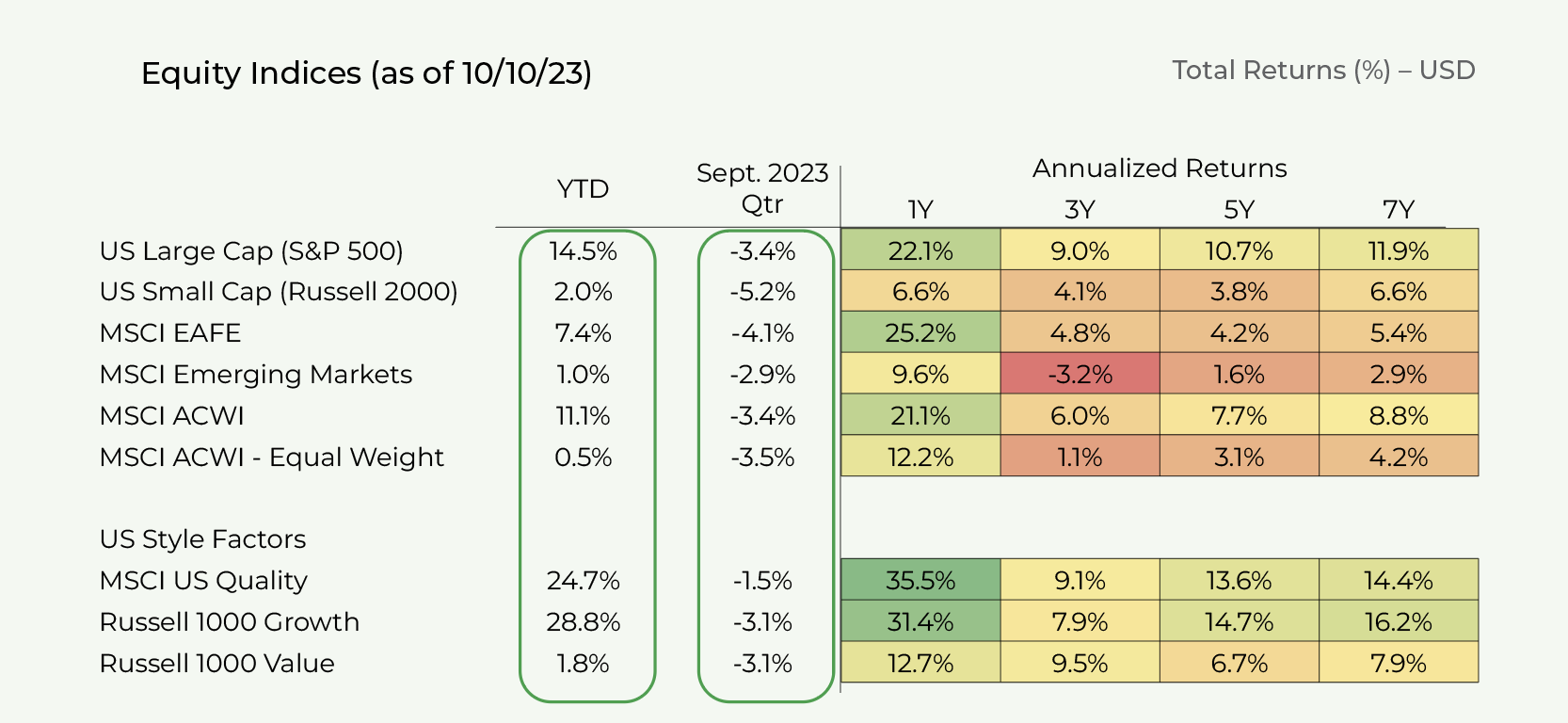

Global equity markets (MSCI ACWI Index) declined by 3.4% during Q3 but remain up 11.2% YTD through Oct. 10, 2023.

During Q3, declines were widespread across regions with most major regions down 3% to 4%.

Globally, value stocks (-1.8%) materially outperformed growth stocks (-4.9%) during Q3. However, on a YTD basis, growth stocks are up 20.7% vs. value stocks up only 2.3%.

Technology (-6.2%) and consumer discretionary (-4.9%) stocks underperformed during Q3 but have performed well YTD (+32.4% and +18.3% respectively). Communication services stocks which have a high digital and internet presence were up +0.5% in Q3 and are up 30.1% YTD.

Defensive sectors such as utilities, consumer staples and healthcare performed poorly in the quarter and were down -8.6%, -6.2% and -2.7% respectively. YTD, these sectors were down -10.0%, -3.8% and – 0.9% respectively.

Cyclical sectors posted mixed performance during Q3 with the energy sector up +10.7%, financials down -0.9% and industrials down -5.2%. YTD, these sectors have trailed the broader market (+11.2%) with energy +6.5%, financials +2.9% and industrials +8.4% respectively.

US large-cap equities (S&P 500) were down 3.4% during Q3 but remain up 14.5% YTD.

The YTD performance is deceptive however and has been driven by a select group of technology, consumer discretionary, and internet stocks (the Magnificent Seven comprised of Nvidia, Apple, Microsoft, Alphabet, Meta, Amazon and Tesla).

On an equally weighted basis (as opposed to market-cap weighted), the S&P 500 is only up 2.2% YTD.

These seven stocks now comprise 29.6% of the market cap of the S&P 500 (eclipsing the 29.1% peak seen in 2021).

The US S&P technology and consumer discretionary sectors gave back some gains in Q3 (-5.7% and -4.8% respectively) as interest rates increased and some of the AI excitement dissipated. However, they are still up 39.5% and 27.9% YTD.

In the US, energy was the best S&P sector performer in Q3 at +12.2% as oil prices rallied driven by unexpected OPEC supply reductions. YTD, however, S&P energy is up 3.8% and has significantly trailed the broader S&P 500 (which rose +14.5%).

US small cap stocks performed worse than large caps and were down 5.1% in Q3 and are only up 2.0% YTD as investors are concerned that higher interest rates and the effects from a potential recession would have a greater impact on small-cap earnings than on large cap stocks.

Additionally, small-cap stocks tend to have higher leverage and may experience declining profits resulting from sharp increases in borrowing costs.

International developed stocks (MSCI EAFE) were down 4.1% during Q3 and up 7.4% YTD in USD.

The quarterly declines were primarily driven by the -5.1% return of European equities. Europe’s macroeconomic fundamentals continued to weaken, especially in Germany.

Emerging markets were down 2.9% during Q3 and +0.9% YTD.

Chinese equities were down 1.9% during the quarter and are down 8.0% YTD. The underperformance was driven by a sharp slowdown in China’s nascent post-COVID recovery coupled with continued concerns regarding the country’s embattled property development sector.

We anticipate that China will increase its stimulus efforts during Q4 2023 and during 2024, which could provide uplift to Chinese equities and emerging markets broadly.

On a YTD basis, EM performance has essentially consisted of divergent China and non-China stories. Chinese equities (33% of index) are down 8% YTD while most other EM countries such as India, Taiwan, Korea, Brazil and Mexico have all delivered positive

returns (with Mexico and Brazil delivering +12% returns).

Analysts are forecasting an improving trajectory for US corporate earnings (S&P 500) beginning with Q3 2023 and accelerating into 2024.

S&P 500 earnings declined 4.4% during H1. Analysts are forecasting flat growth in Q3 2023, 9.4% in Q4 2023, and 12.0% growth in 2024. Notably, as confidence regarding achieving a soft landing has increased, the number of positive analyst earnings estimates revisions has increased steadily.

We believe the outlook for 2024 corporate earnings remains quite uncertain. On the one hand, certain sectors are experiencing resumptions in demand, manufacturing surveys are improving, input and other cost inflation has subsided, and consumer spending remains strong. On the other had, the economy could stall as the effects of higher interest rates ripple through with a lag, especially once excess pandemic savings are largely depleted. Additionally, the risk of spillover from weakening European macroeconomic conditions or an unexpected geopolitical event remains high.

For investors with a mid-term time frame, we continue to believe that stocks of high-quality companies will outperform given their strong business models, superior revenue and earnings growth and strong returns on capital.

However, given the massive YTD outperformance of growth stocks (especially technology stocks that have benefitted from AI sentiment), we would not be surprised to see value stocks outperform over the next 6-9 months (or at least more balanced performance between growth and value).

The NASDAQ 100 and Russell 1000 Growth indexes are up 39.2% and 28.8% YTD. Valuations have increased and are well above historical norms.

While technology stock price performance did decline in Q3 as treasury yields appreciated sharply, the test for technology-oriented growth stocks remains in terms of Q3 earnings releases and commentary. These stocks may be susceptible to a pullback should AI be less of a near-term revenue and earnings driver than currently expected by investors.

Certain value stocks such as financials have materially underperformed YTD, and valuations appear attractive. Bank stocks may rebound if loss provisions remain relatively low and CEO commentary regarding the macro economy becomes more bullish. Energy stocks may continue to rally if oil prices strengthen due to ongoing volatility in the Middle East.

Valuation

Equity markets are generally fairly valued relative to historical averages with US markets modestly overvalued and international developed markets modestly undervalued.

In the US, equity market valuations are expensive relative to government bonds.

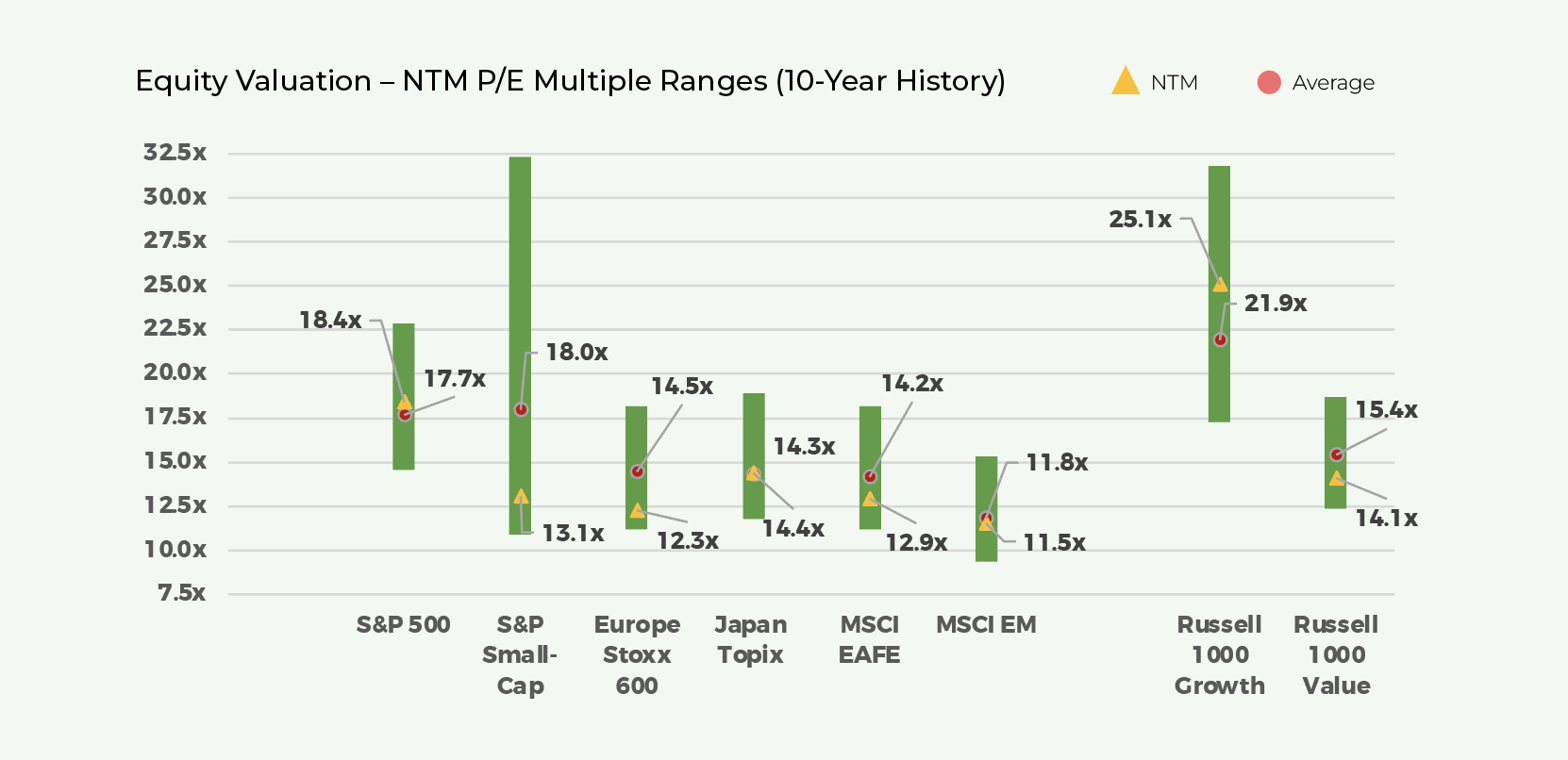

The S&P 500 presently trades at 18.4x consensus NTM earnings (which may be too high)

Historically, the S&P 500 earnings yield (inverse of multiple) has averaged 200-300bps over 10-Year Treasuries.

With 10-year Treasuries yielding 4.6%, at first glance, a 13.5x-15.5x forward EPS multiple is “fair” for the S&P 500 based on relative valuations to bonds.

However, most investors do not expect the 10-year Treasury to remain at 4.6% for an extended period of a time. If the 10-year was to retreat to 3.5%, a fair valuation of 15.5x-18.0x forward EPS is more reasonable.

Additionally, our mid-term return outlook for risky corporate credit (high yield bonds and leveraged loans) is similar to that for equities, with lower risk.