Asset-based lending consists of senior loans that are secured by hard or financial assets. These assets include equipment, inventory, accounts receivables, and royalties among others across a variety of industries.

Borrowers may include corporations or individuals, or even lenders who lend to these borrowers.

Borrowers may seek asset-based loans for several purposes including acquisitions, recapitalizations or refinancing, bridge financing, and general corporate growth. Cash constrained borrowers may turn to these loans as a form of rescue financing during periods of stress.

When the borrower is another financial lending institution, the collateral includes pools of underlying assets.

These pools could be further segregated into lower-risk senior and higher risk junior tranches.

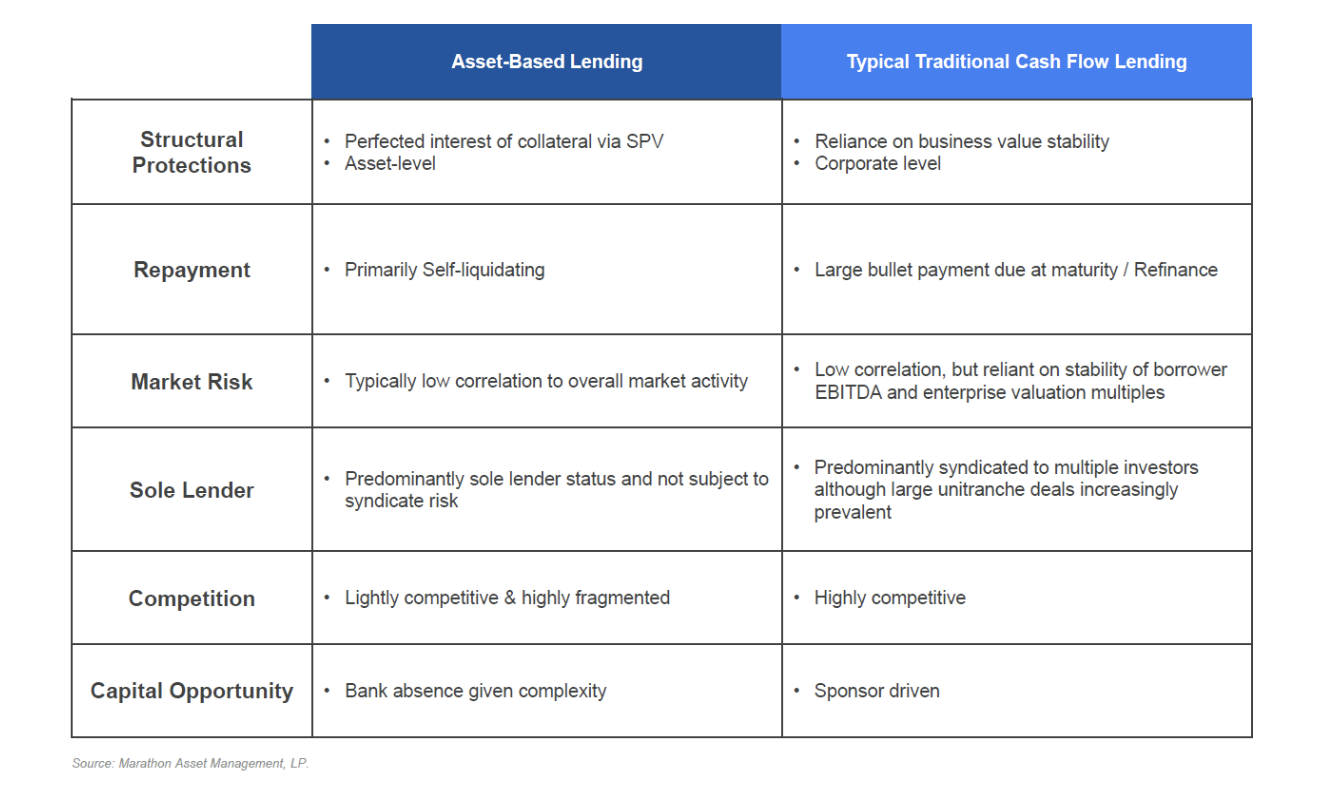

The loan-to-value (LTV) of asset-based loans is based on the liquidation value of the collateral. This is different from corporate cash-flow based direct lending where the loan-to-value is based upon the enterprise value of the business.

Recovery of asset-based loans is dependent upon the value of the borrowers’ assets and not on their financial performance (i.e. EBITDA and Enterprise Value).

The market size for asset-based lending is very large at an estimated $30 Trillion.

Large sectors include residential mortgage loans, healthcare loans and royalties, transportation loans and leases, corporate asset-based lending, consumer loans, and commercial real estate loans.

Differences Between Asset-Based Lending and Cash-Flow Lending

Attractiveness of Asset-Based Lending

Strong cash flow generation with predictable income.

Asset-based lending strategies generate high levels of coupon income with higher cash flows as the loans amortize during their life (as opposed to corporate cash flow loans which have bullet amortizations upon maturity).

High complexity drives excess spread and better structural protections.

Given the expertise relied to assess collateral of individual or pooled borrowers and the complexity involved in asset-based structures, spreads tend to be higher relative to corporate cash-flow lending.

Private asset-based loan spreads may be 150bps-300bps higher for the same level of seniority relative to corporate direct lending.

Additionally, structural protections are better as collateral is clearly defined and lenders can enact stricter covenants and stronger documentation.

Asset-based lenders have much more real-time access to data (weekly or bi-weekly) and can take pre-emptive measures to rectify performance faster than corporate direct lenders (quarterly statements in most cases).

High diversification and low correlation compared to corporate cash-flow-based investments.

Large number of individual positions with a wide variety of collateral types.

Collateral values tend to be less volatile than corporate enterprise values. Additionally, collateral values are generally uncorrelated to enterprise values.

Less efficient markets drives higher potential for alpha.

Incumbent managers with sectoral expertise and deep relationships have sourcing advantages.

Many more opportunities to drive excess return or mitigate risk through structure design.

Asset-Based Lending Investment Opportunities

Asset-backed credit solutions are seeing increased demand as companies seeking liquidity are pledging high-quality sources of collateral such as receivables, inventory, and certain fixed assets.

BCA believes that asset-lending funds nicely complement corporate direct funds in investors’ private credit portfolios.

In evaluating asset-based private credit managers, BCA assesses the following:

Expertise in certain asset-based categories such as receivables, inventory, consumer-backed loans, commercial real estate, etc.

Examples include White Hawk (receivables and inventory), Canyon (real estate). Marathon (multi-sector), and Atalaya (consumer)

Historical track record across credit cycles and underwriting performance (i.e. realized losses).

Depth of relationships and opportunities for competitive sourcing advantages.

Covenants, strengths of legal documents, protection afforded under asset-based structures (i.e. – level of collateral losses before impairments occur).