Performance

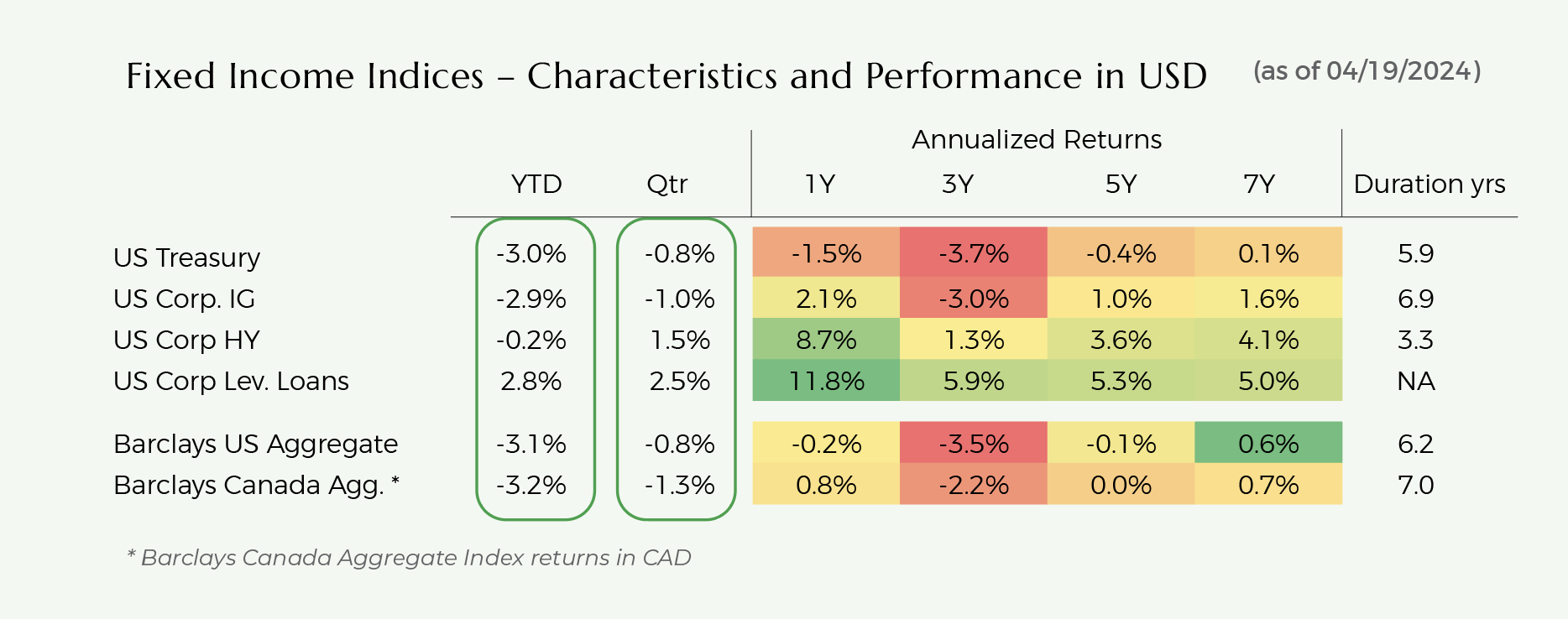

Safe fixed income (government bonds and corporate investment grade bonds) declined modestly during Q1, with declines further intensifying since quarter end.

US Treasury yields appreciated gradually through Q1 and then swiftly moved upwards since quarter-end.

Yields moved up 30bps-40bps across the Treasuries curve during Q1. Since quarter-end, yields have appreciated another 30bps-40bps through April 19th.

The sharp increase in yields since quarter-end was driven by unfavorable inflation data (inflation not falling as much as expected) and continued strong economic data in terms of consumer spending and employment.

Both high yield bonds and leveraged loans appreciated strongly in Q1. However, high-yield bonds have declined since quarter-end as rates have risen.

HY bonds benefitted from high coupon rates and modest spread tightening in Q1. Since quarter-end, the performance reversal has been driven by rising interest rates and modest spread widening.

CCC-rated (the riskiest) high-yield bonds have continued to outperform the broader high-yield index YTD.

Leveraged Loans (floating rate) have benefitted from high coupon rates (SOFR at 5.3% throughout 2024 while spreads have remained stable).

Valuation

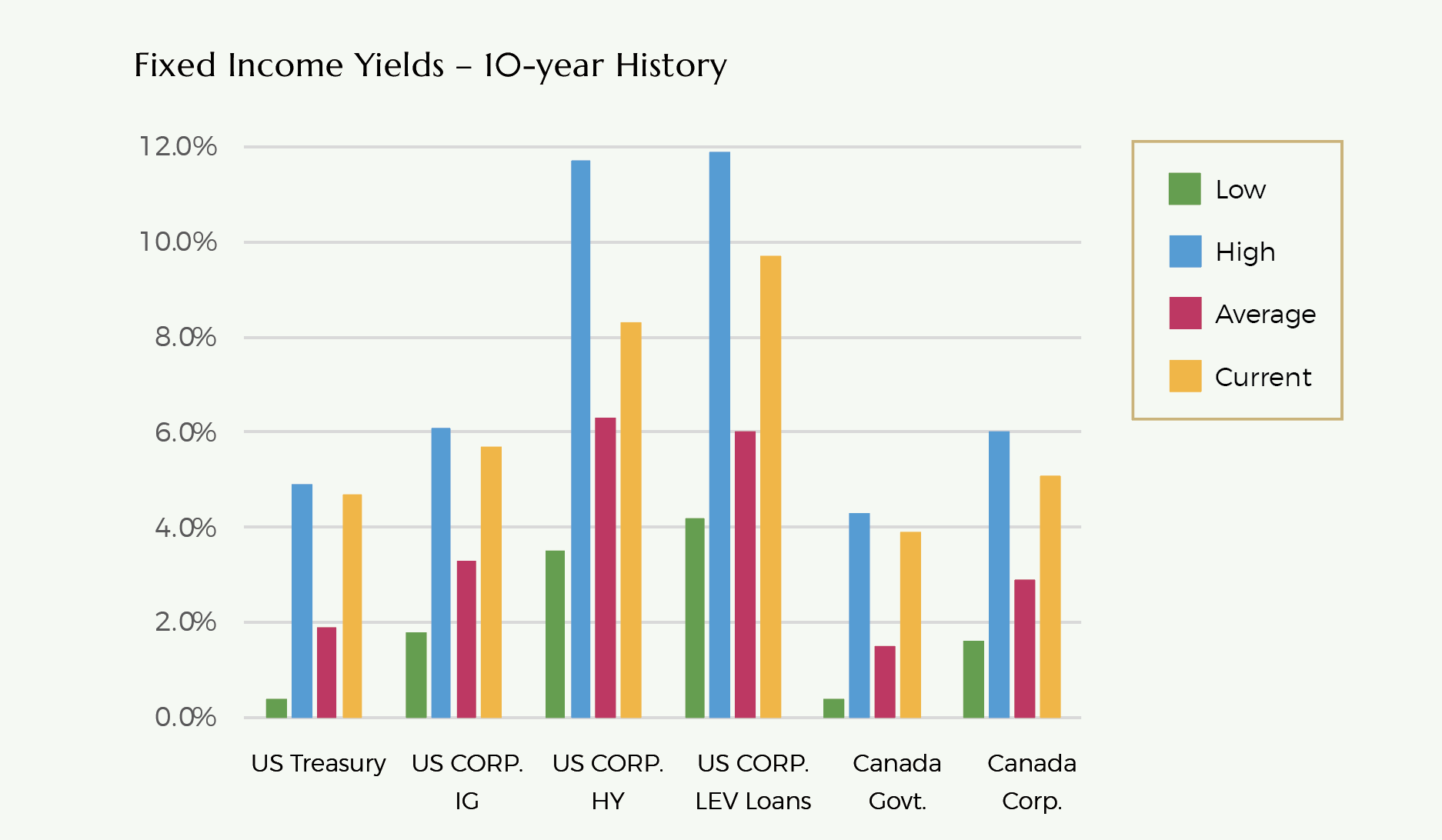

Safe fixed income (government bonds and investment grade corporate bonds) yields have risen sharply and are now at highly attractive levels.

US Treasuries are yielding roughly 5.2%, 5.0% and 4.6% for 1-year, 2-year, and 10-year maturities.

US corporate investment grade bonds are now yielding 5.6% (with risk of default very low).

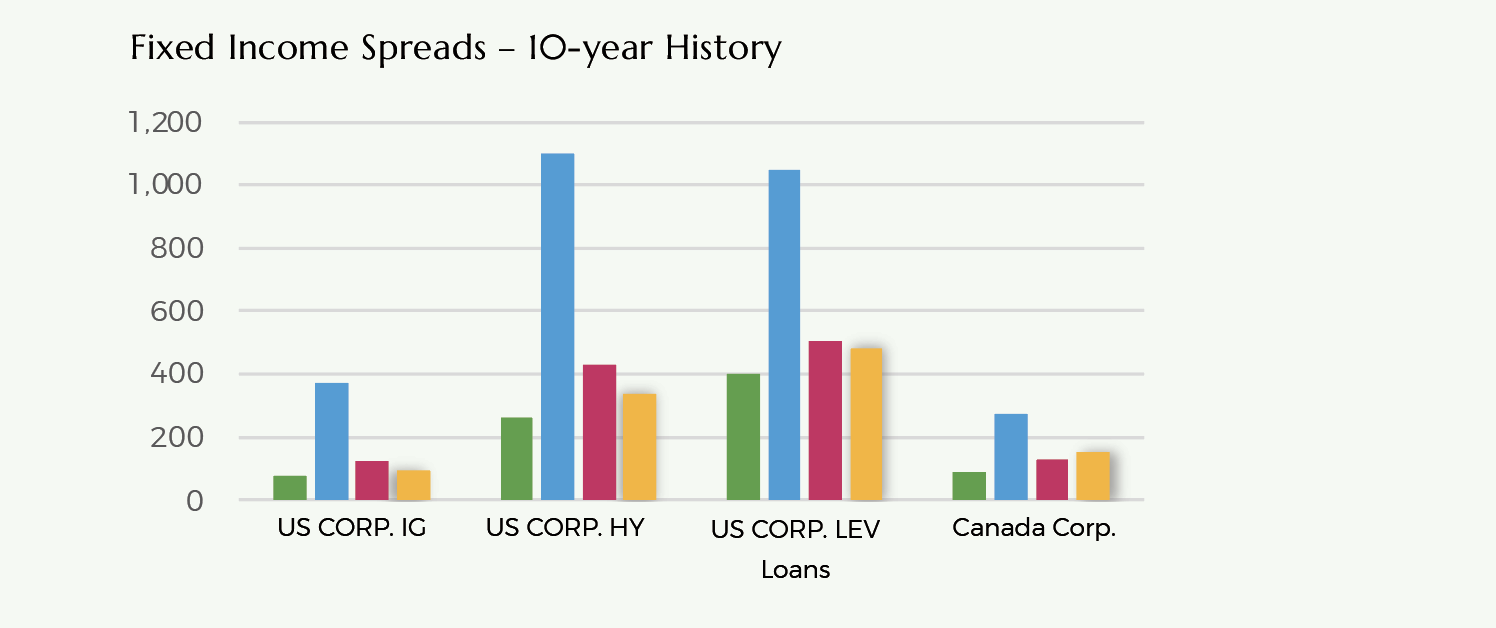

Both investment grade and high-yield bond spreads remain tight reflecting strong corporate earnings performance despite rising rates.

IG spreads are presently at 92bps and HY spreads are at 323bps. These levels are well lower than 10-year averages of 125bps and 425bps respectively.

Spreads have generally widened further during prior recessionary periods (200bps for corporate bonds and 800bps for HY bonds).

However, the quality of the high yield index is much stronger now than in previous periods. When coupled with today’s high base rates, it is unlikely that spreads will widen to those experienced in previous recessions (even if economic activity slows substantially).

Access to credit varies considerably depending upon borrower type.

Large corporate borrowers have ample access to credit availability via banks or through large private lenders.

Following a pause in late 2022 through mid-2023, large banks have increasingly re-entered the leveraged loan market and new issuance spreads in the large end of the market have contracted by 125bps to 150bps.

On the other hand, lower-middle-market and middle-market companies are facing constraints regarding access to capital.

Regional banks have pulled back substantially from lending to these companies. As such, spreads to these borrowers have not contracted as much (only 50bps-75bps) relative to the larger borrowers.