INTRODUCTION

BCA Approach to Portfolio Design & Construction

At BCA, our client families have long time horizons, often multi-generational. Accordingly, we aim to construct portfolios that perform predictably over the long term with resilience in the interim to ever-changing economic and market conditions. Our investment team applies its collective, first-hand expertise across multiple asset classes to develop well-informed views on the role each asset class can play in a diversified portfolio based on its specific investment attributes. This guides our strategic asset allocation—the mix and weights of each asset type across a portfolio. And our granular implementation seeks to enhance each asset class’s virtues through strategy and manager selection.

We follow an endowment-style approach to portfolio construction, one aspect of which means expanding beyond publicly-traded stocks and bonds to incorporate alternative investments, most importantly private equity, credit and real assets. This strategy seeks to outperform the traditional 60/40 stock-bond portfolio with lower risk, driving sustainable long-term growth. It is particularly well suited for ultra-high net worth clients, offering the benefits of a sophisticated, institutionally-inspired investment framework.

We design each portfolio to support a client’s unique financial objectives, ensuring it reflects their projected cash flows, liquidity needs, and risk tolerance. Additionally, we account for any concentrated (public or private) positions that may be specific to their holdings. Once these core factors are established, we construct the broader portfolio, selecting additional asset classes using our seven-year strategic return forecasts as a guiding framework.

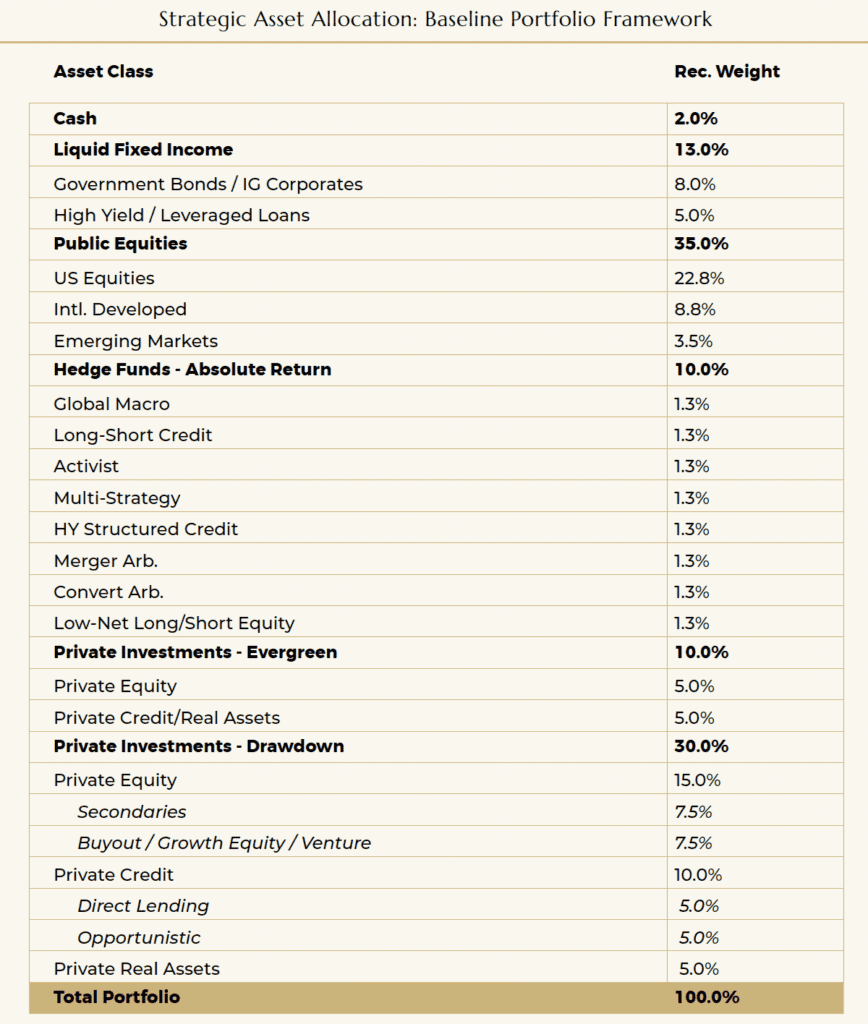

The following table illustrates a possible starting point before accounting for the types of client-specific factors mentioned above.

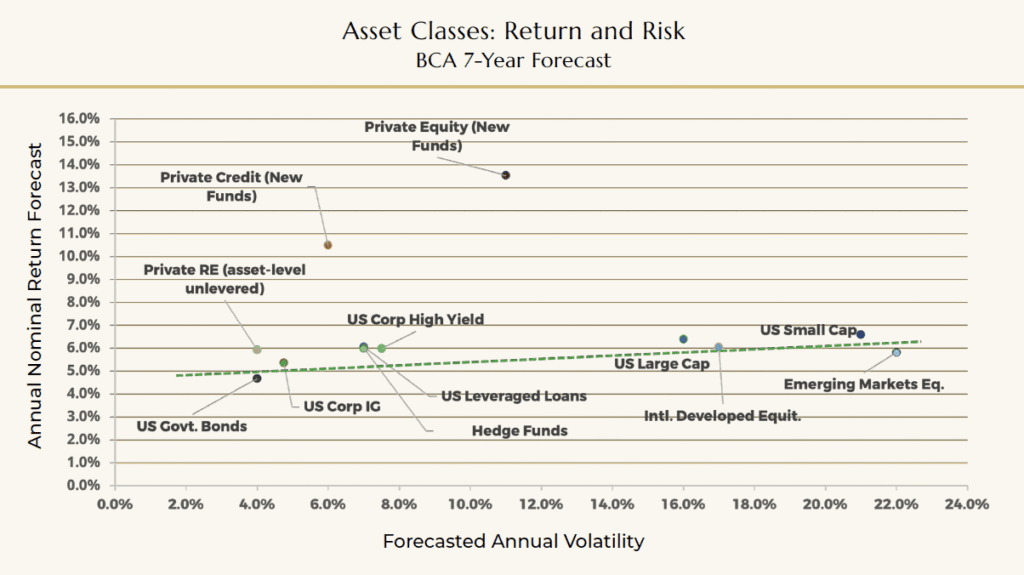

Our investment process is grounded in a rigorous, data-driven methodology, integrating detailed, asset-specific fundamentals to develop precise capital market assumptions. This disciplined approach allows us to optimize asset allocation while balancing risk and return in a way that is both forward-looking and tailored to each client’s financial landscape.

Illustrating some of those assumptions, the following chart presents BCA’s forecasted seven-year returns for various asset classes as of March 2025. These forecasts reflect benchmark-level expectations, not those for individual strategies or managers.

A thoughtfully designed, tightly executed private investment program lies at the heart of our endowment-style approach. As with all asset classes, we have a distinct view on how to build private equity (PE) and private credit (PC) portfolios to enhance long-term results. We research and select top-tier fund managers globally through the lens of our strategic approach. This white paper explores our insights and approach to private investments.

Role of a Private Investment Program in a Diversified Portfolio

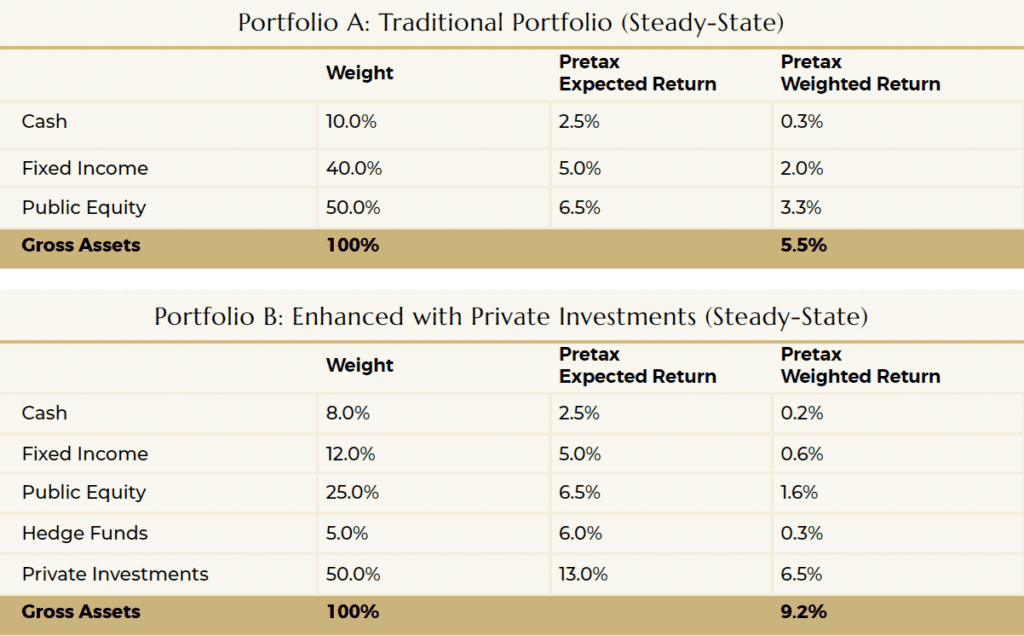

Private investments are designed to enhance BCA portfolios by boosting returns and reducing volatility relative to a more traditional portfolio. Specifically, at steady-state (6-8 years after initiation), as shown below, we would expect a portfolio with a private investment program comprising 50% of the total portfolio to deliver 9.2% annualized returns compared to 5.5% for a traditional equity-fixed income portfolio – in both cases, based on our current capital markets assumptions and the value added BCA expects in our strategy and manager selection.

Private investments also contribute to portfolio stability by smoothing overall returns and reducing drawdowns, as seen during the public equity market corrections of 2022. This enhances long-term wealth compounding. Additionally, private equity (PE) investments may offer significant tax efficiency, as the majority of returns—realized upon exits—are treated as long-term capital gains. This is particularly valuable given the substantial effective cash yield generated by a PE program once it reaches a steady state.

Private Investments: An Attractive Asset Class

Both Private Equity (PE) and Private Credit (PC) have outperformed their public market counterparts over the long term.

Private Equity (PE)

Over the past 30 years, PE has outperformed public equities by 500 basis points annually. The higher returns largely reflect the fundamentally less efficient nature of private markets. Unlike public stocks, which trade on highly liquid exchanges with readily available information, private markets comprise a far greater number of companies with significantly less transparency.

Several fundamental advantages contribute to PE’s higher returns:

- Lower Entry Valuations – Private companies are often acquired at more attractive prices compared to publicly traded firms.

- Operational Improvements – Fund managers seek to actively improve business operations over multiple years, free from the pressure of quarterly earnings reports and market speculation.

- Leverage Utilization – PE funds attempt to prudently use debt to enhance returns.

PE Liquidity Trade-Off & Risk Perspectives

An important risk consideration also drives the return premium of private equity relative to public markets – lower liquidity. Investors in a PE fund must commit capital upfront and fulfill all capital calls when required. Investors realize returns through distributions, which occur when the fund exits its investments. The size and timing of both capital calls and distributions are unpredictable and driven by market conditions and the discretion of the fund manager.

While private investments lack liquidity, they offer certain attractive risk characteristics:

- Less Volatility – Unlike publicly traded stocks, which react to short-term market swings, PE valuations tend to reflect long-term business fundamentals. Fund managers (“sponsors”) use valuation methods that emphasize operational trends rather than daily market fluctuations.

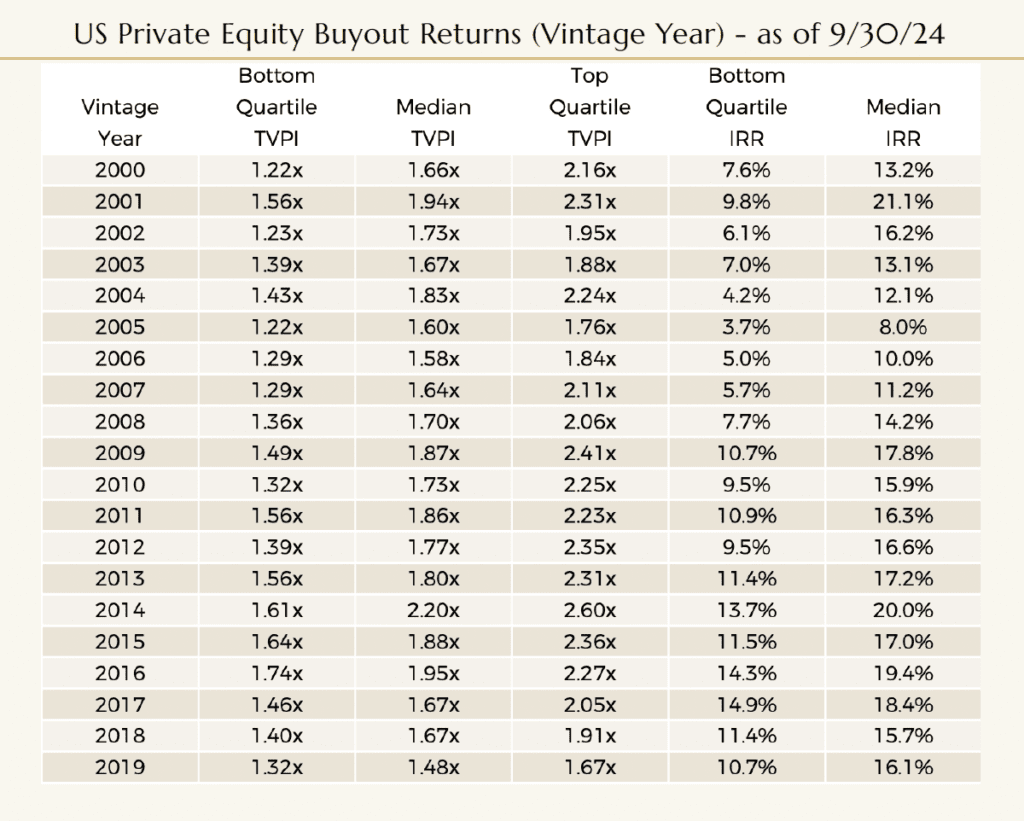

- Resilient Returns – As shown in the following table, even the lowest-quartile private equity funds have historically delivered positive returns over their full lifecycle, including those launched in challenging periods (e.g., just before the Global Financial Crisis).

The table also highlights the performance dispersion among private equity (PE) managers, especially in comparison to public equity managers. Top-quartile PE managers can exceed median returns by 500 to 1,000 basis points annually, making the selection of managers crucial. We see this as an opportunity—skilled allocators like BCA can create value by identifying strategies and managers that are more likely to outperform.

Private Credit (PC)

Private credit refers to lending conducted outside the traditional banking system and public high-yield debt markets. Private lenders work directly with borrowers to negotiate and originate loans that are closely held by the originators and not traded on public exchanges.

Since the Global Financial Crisis (GFC), increased banking regulations and capital requirements have led traditional banks to scale back lending to certain borrowers. As a result, private credit has expanded significantly, growing from $500 billion in 2015 to $1.6 trillion today, filling the gap left by banks.

Key Characteristics & Advantages

Private credit primarily includes senior and mezzanine (junior) loans to corporate borrowers, as well as asset-backed loans, where specific collateral secures the obligation. Compared to publicly traded debt (also called broadly syndicated loans), private credit offers higher yields. Loans typically earn 150 to 300 basis points higher spreads for similar credit quality. Borrowers accept these higher costs in exchange for certainty of execution, simplified negotiations with a single lender instead of a large, syndicated group, and access to financing that might not be available through public markets.

Additionally, private credit loans have tighter covenants, or contractual restrictions, which provide better risk control for lenders compared to public credit markets.

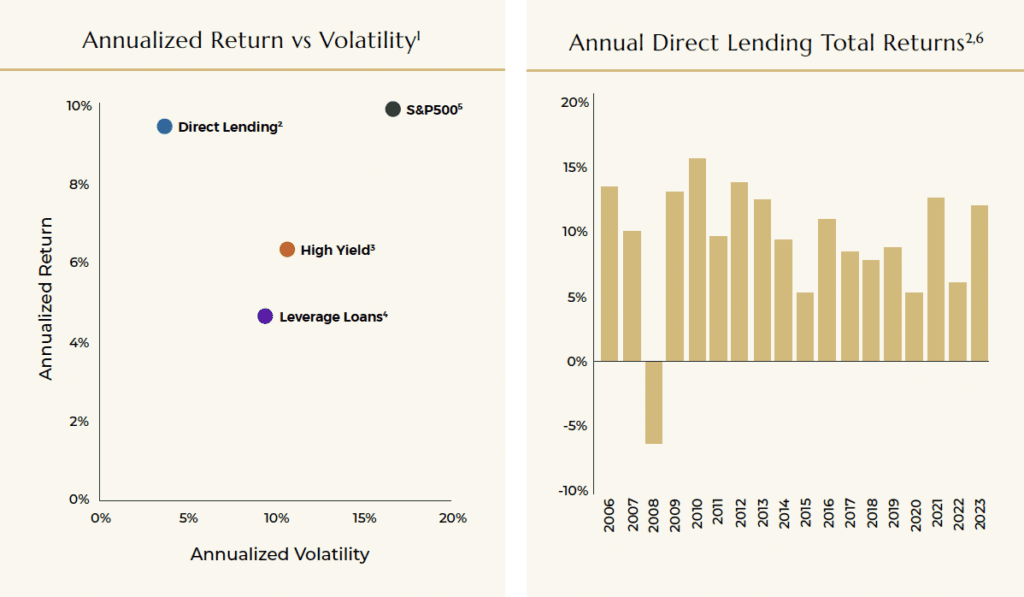

Performance & Volatility

As shown in the following charts, private credit, as measured by the Cliffwater Direct Lending Index, has outperformed high-yield bonds and leveraged loans by 250 to 400 basis points annually since 2006. It also exhibits lower volatility than publicly traded debt because privately held loans are not subject to daily mark-to-market fluctuations seen in public credit markets.

1 Represents the annualized return of the indices, where return is defined as gross income return, net realized gains (losses), and net unrealized gains (losses), and volatility defined as the standard deviation of quarterly index returns from 12/31/2005 through 12/31/23 for all indices. 2 Direct Lending is represented by Cliffwater Direct Lending Index (CDLI) as of December 31, 2023. 3 High Yield is represented by Credit Suisse High Yield Total Return Index. 4 Leveraged Loans is represented by Credit Suisse Leveraged Loan Total Return Index. 5 S&P 500 is represented by the S&P 500 Total Return Index. 6 Total return is defined as gross income return, net realized gains (losses), and net unrealized gains (losses) and is prior to any fees and expenses. BCA’s Approach to Private Investments

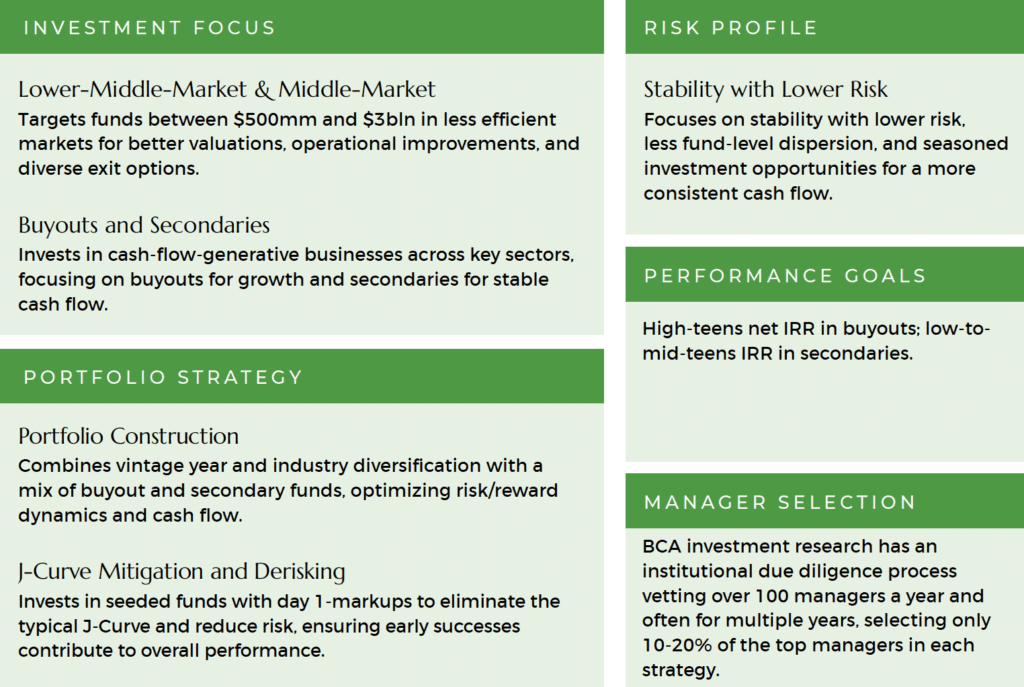

To drive higher returns in both private equity (PE) and private credit (PC), we focus on funds operating in the less-trafficked middle-market and lower-middle-market segments.

We believe these markets provide more attractive valuations and pricing, offering multiple pathways to value realization.

Private Equity

In private equity, the sources of higher returns vary across different strategies.

For buyout and growth equity strategies, we seek fund managers with superior sourcing capabilities and a proven track record of successfully executing value creation strategies. These managers drive returns through operational improvements, including revenue growth, cost management, capital expenditures, and strategic tuck-in acquisitions.

In the secondary market, we focus on fund managers with information advantages and strong underwriting expertise in evaluating mature portfolio companies, ensuring well-informed investment decisions and optimized risk-adjusted returns.

The performance goals outlined in the table represent our expected outcomes based on our investment strategy and focus. These goals are informed by our experience and reflect the anticipated benefits of our disciplined approach to portfolio construction and asset allocation.

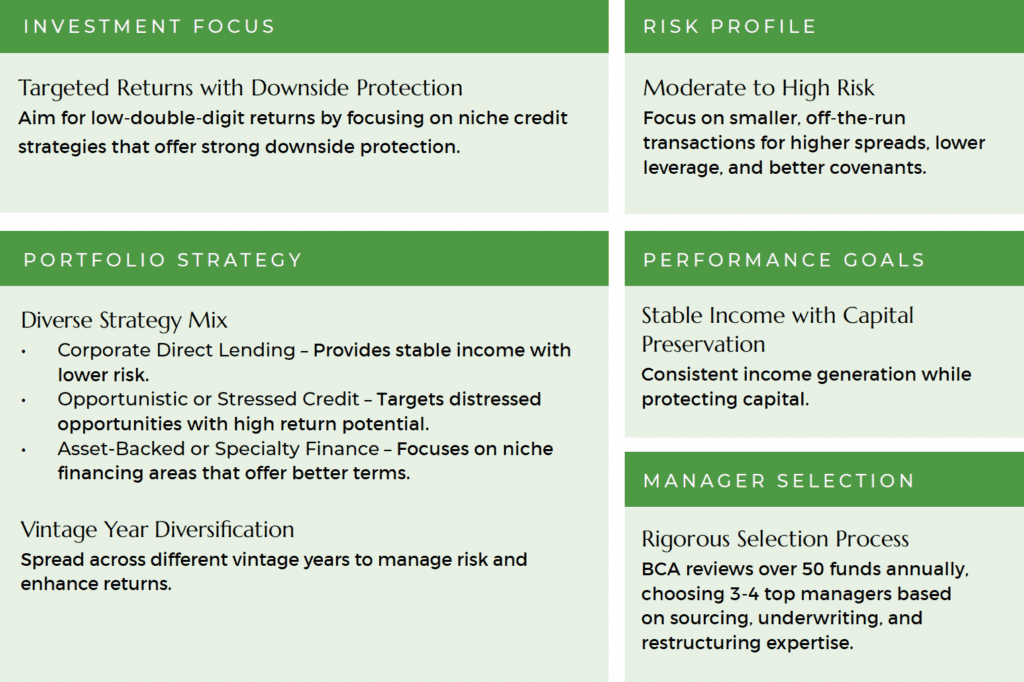

Private Credit

In private credit, we focus on key attributes that align with our investment objectives of stable income and capital preservation. We target funds specializing in smaller, off-the-run transactions that offer higher spreads, lower leverage, and stronger covenants—providing enhanced risk-adjusted returns.

Our approach incorporates a diverse mix of private credit strategies:

- Corporate direct lending for stability and consistent income.

- Opportunistic credit to capitalize on higher-returning distressed situations.

- Asset-backed specialty finance, which generates returns from alternative sources of risk.

Across all strategies, we prioritize fund managers with exceptional credit underwriting expertise and a strong emphasis on downside protection, ensuring investments are backed by robust cash flows or asset value coverage. These managers possess deep knowledge of collateral and enforce strict documentation and covenants to safeguard capital.

Fund Selection and Timing

In both private equity and private credit, we focus on fund sizes between $500M and $3B, a range that provides strong return potential while maintaining operational efficiency. BCA’s size is a strategic advantage in this space. Unlike large brokerage and private banking platforms, we are not constrained to investing in mega funds, where many value-enhancing dynamics are diluted. At the same time, by aggregating capital across our clients, our investment commitments are large enough to make BCA a meaningful investor in middle-market funds.

Strategic Late-Stage Fund Investments

A distinct aspect of BCA’s approach is our preference for investing in funds late in their fundraising process, shortly before final close.

In private equity, this late-close strategy provides several key benefits:

- Reduced “Blind Pool” Risk – With 20-40% of capital already deployed, we gain valuable insight into the fund’s early performance and portfolio composition, reducing uncertainty.

- Immediate Net Asset Value (NAV) Markups – Investors benefit from an instant uplift in portfolio valuation.

- Enhanced Internal Rates of Return (IRRs) – The J-Curve effect is significantly mitigated, improving reported performance.

- Faster Capital Deployment – Funds are already actively investing, reducing cash drag.

- Shorter Time to Steady-State – Private investment portfolios mature more quickly.

By leveraging this approach across all PE and PC strategies, we maximize returns while mitigating common risks associated with private investment vehicles.

Private Investment Fund Dynamics: The Need for a Program

Most private investment funds operate as drawdown vehicles, meaning their investment and cash flow patterns differ significantly from traditional investments. When an investor commits capital to a private fund, the fund manager calls capital incrementally as investment opportunities arise, rather than deploying the full commitment upfront.

As these investments mature and are eventually exited, the fund returns capital to investors in the form of cash distributions. This staggered capital deployment and return cycle is why it is so importance to have a well-structured investment program to ensure consistent exposure to private investments over time.

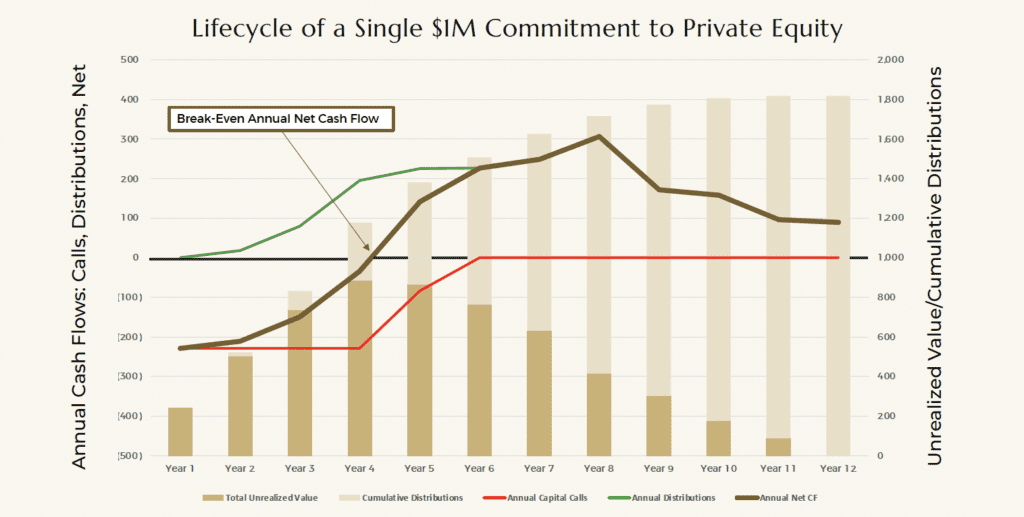

Capital Flow Dynamics of a Typical PE Buyout Fund

- Capital Calls Before Distributions

Investors fund capital calls in the early years, with net cash flow turning positive around year four or five as both calls trail off and investments are exited with proceeds distributed. - Return Composition

Unrealized Value – The marked value of held investments, peaking around year five before declining.

Cumulative Cash Distributions – Cash returned as distributions as portfolio companies are sold. - Measuring Returns

Multiple on Invested Capital (MOIC) is a key metric. In this example, MOIC reaches 1.8x over the fund’s lifecycle. - All Returns Become Distributions

By the fund’s end, Unrealized Value reaches zero as all investments are exited.

This last point is crucial. Unrealized Value represents exposure to private investments at any point in time. Because this declines as funds move into their liquidation phase, a Private Investment Program is essential. To build exposure to a targeted allocation and maintain it consistently over time, investors must commit annually to new funds.

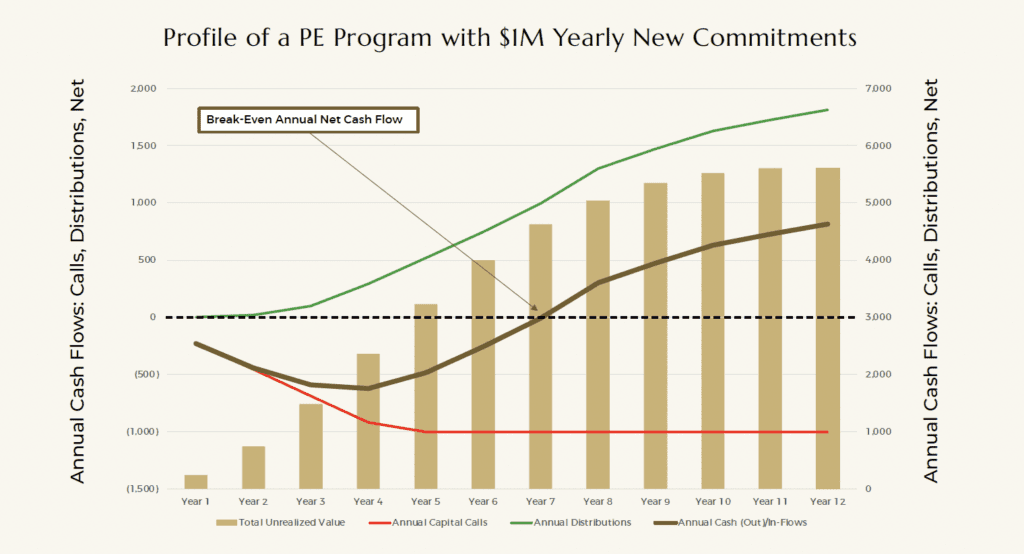

Private Investment Program Dynamics, Generally for PE

- Breakeven Point & Net Cash Generation

Capital calls precede distributions, but by year seven, the program reaches breakeven and becomes a persistent net cash generator. - Steady-State Exposure

Annual commitments to new funds build exposure, measured as Unrealized Value, at approximately $5.5M in the given example and growing more modestly from there. - Self-Sustaining Capital & Yield

Once steady-state is achieved, the program internally funds capital calls using distributions from maturing investments, generates consistent net cash flow — in this example (~$800K annually), effectively yielding ~14% on $5.5M Unrealized Value — and continues to grow Unrealized Value, ensuring sustained exposure to private investments.

This structure allows investors to maintain portfolio exposure, generate income, and recycle capital efficiently over time.

Private Program: Managing Risk

Like all investments, private investments carry risks. Predicting annual vintage performance is speculative, which is why BCA, like institutional investors, recommends consistent annual allocations to ensure vintage year diversification. Additionally, within each vintage, broad exposure across both PE and PC and to multiple strategies within each reduces risk. We believe a well-diversified vintage year of six or more funds across PE and PC has a very low probability of negative returns over its lifecycle.

While private investments enhance returns and lower volatility, they require careful liquidity planning. Managing cash flow is essential, particularly in the early years of a private program. BCA works closely with clients to model and forecast all their inflows and outflows, considering employment, lifestyle and investments. This proprietary model – which is both a forecast of each client’s financial life and key investment planning tool – informs optimal program sizing and strategy allocation. In turn, BCA integrates forecasted private investment cash flows into the broader portfolio planning model.

Given the uncertainty around capital calls and distributions, maintaining a prudent margin of safety is critical.

It is important to assess how the private program is funded in its early years—whether through external income, concentrated asset dispositions, or sales from the diversified portfolio. In particular when relying on portfolio assets, maintaining sufficient liquidity and price certainty is key to avoiding disruptions.

Conclusions

A private investment program is a core component of many BCA client portfolios, providing enhanced return potential, reduced volatility, and sustainable long-term wealth growth. Designed with a well-structured framework, the program is tailored to each client’s unique needs while maintaining a disciplined risk management approach.

BCA continuously seeks compelling opportunities in private markets, with a strong focus on middle-market and lower-middle-market funds ($500M-$3B). We believe our expertise in research and sourcing gives us a competitive advantage in identifying high-quality investments within this space.

In our view, by combining higher expected returns with a smoother return profile, private investments increase the likelihood of achieving targeted portfolio returns over the long term while improving overall portfolio resilience.

Disclaimer: This white paper is based on a combination of historical performance and our judgment. We make no assurances about future performance, as market conditions and investment outcomes may vary.