Performance

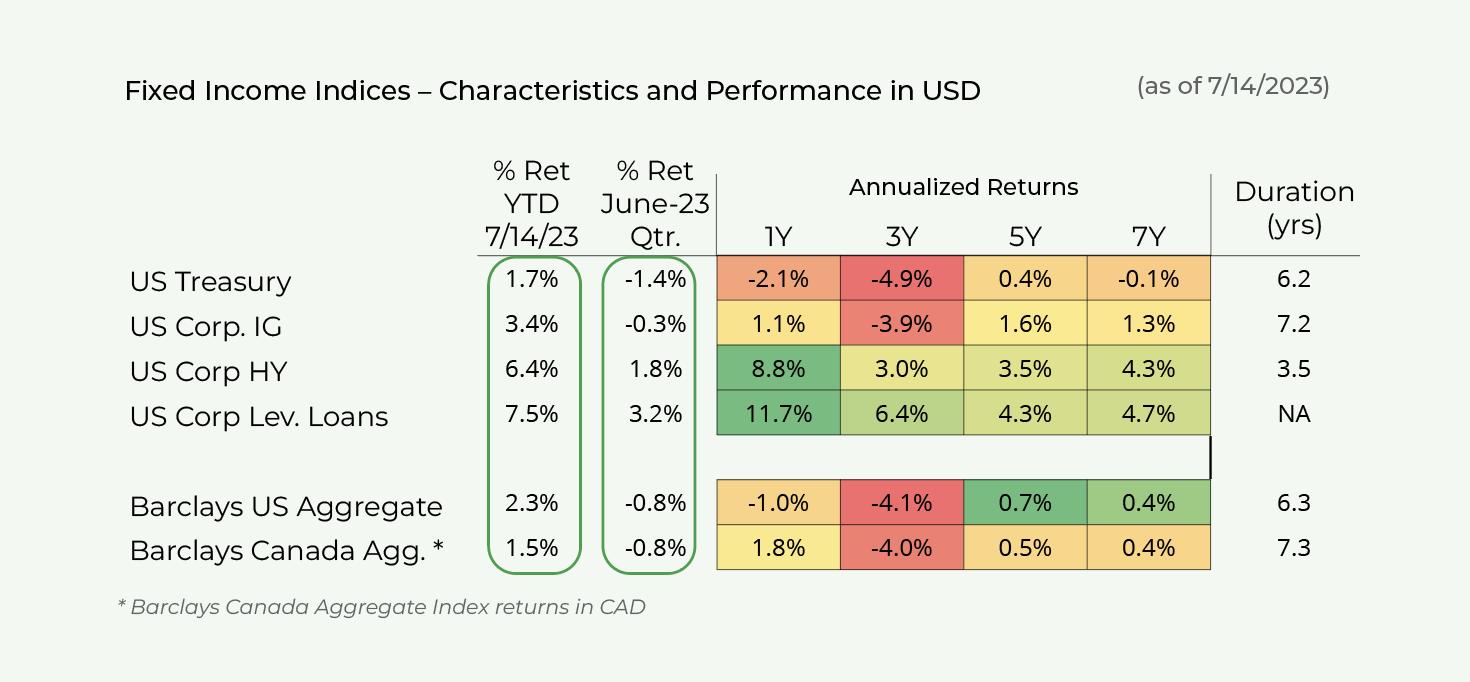

Safe fixed income (government bonds and corporate investment grade bonds) declined modestly during Q2 as interest rates increased.

Following a swift fall during March post the SVB crisis, interest rates generally increased as economic activity and job market data surprised to the upside.

2-Year US Treasury yields increased from 4.2% to 4.8% presently and 10-year yields increased from 3.5% to 4.1% briefly before retreating to 3.8% presently.

However, US Inflation has continued to moderate with June headline CPI increasing only 0.1% MOM and 3.0% YOY. Core inflation increased 0.2% MOM and 4.8% YOY, down sharply from its Sept. 2022 6.6% peak.

Both high yield bonds and leveraged loans have appreciated YTD.

Both HY bonds and leveraged loans benefitted from high current income and price appreciation from tightening spreads.

CCC-rated (the riskiest) high-yield bonds have performed best thus far this year (+11.6%) despite bankruptcy filings reaching the highest levels since the GFC.

Valuation

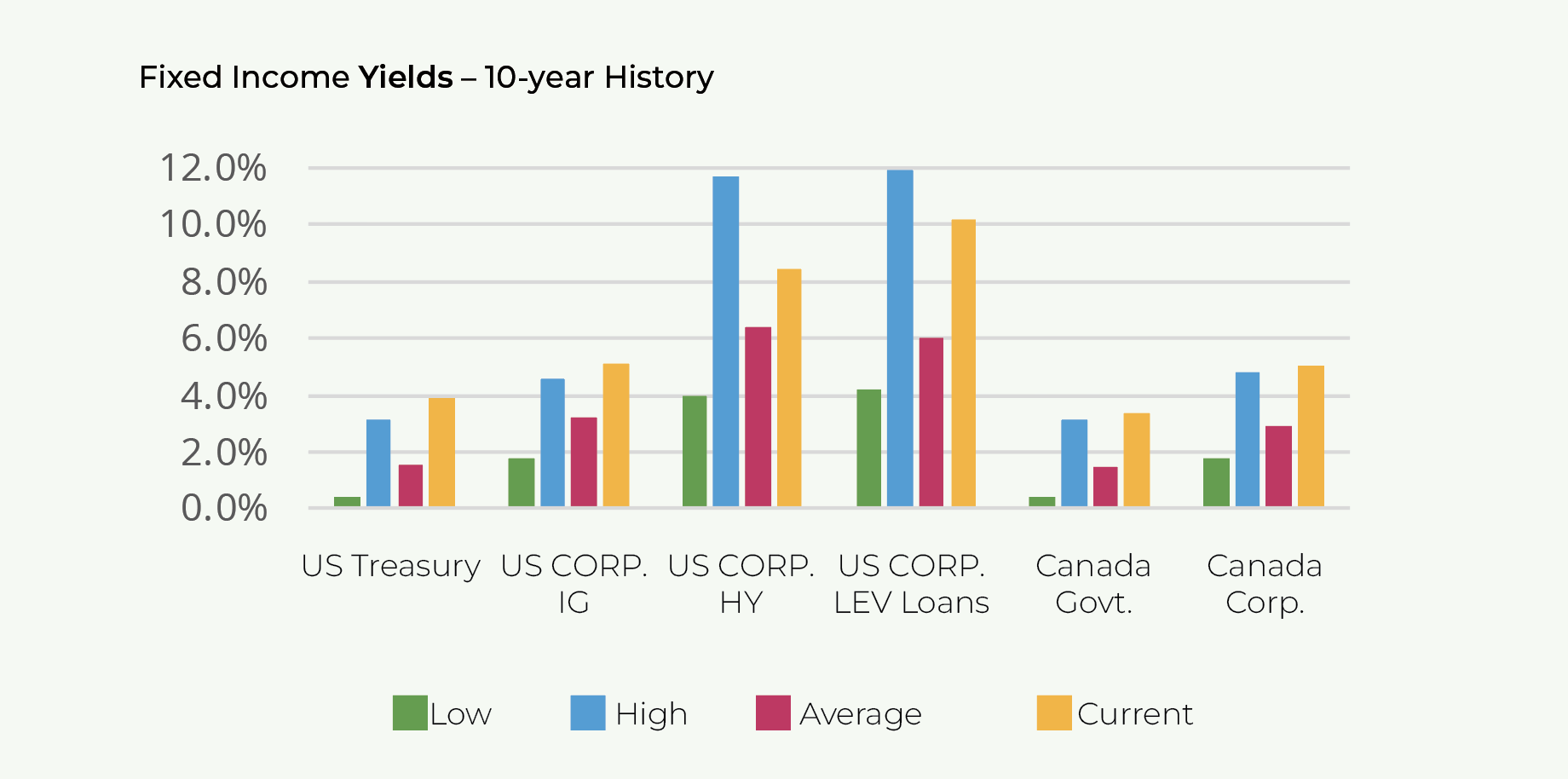

Safe fixed income (government bonds and investment grade corporate bonds) yields remain at attractive levels.

US Treasuries are yielding roughly 4.8%-5.3% for 1-to-2-year maturities and 3.8% for 10-year maturities.

US corporate investment grade bonds are now yielding 5.3% (with risk of default very low).

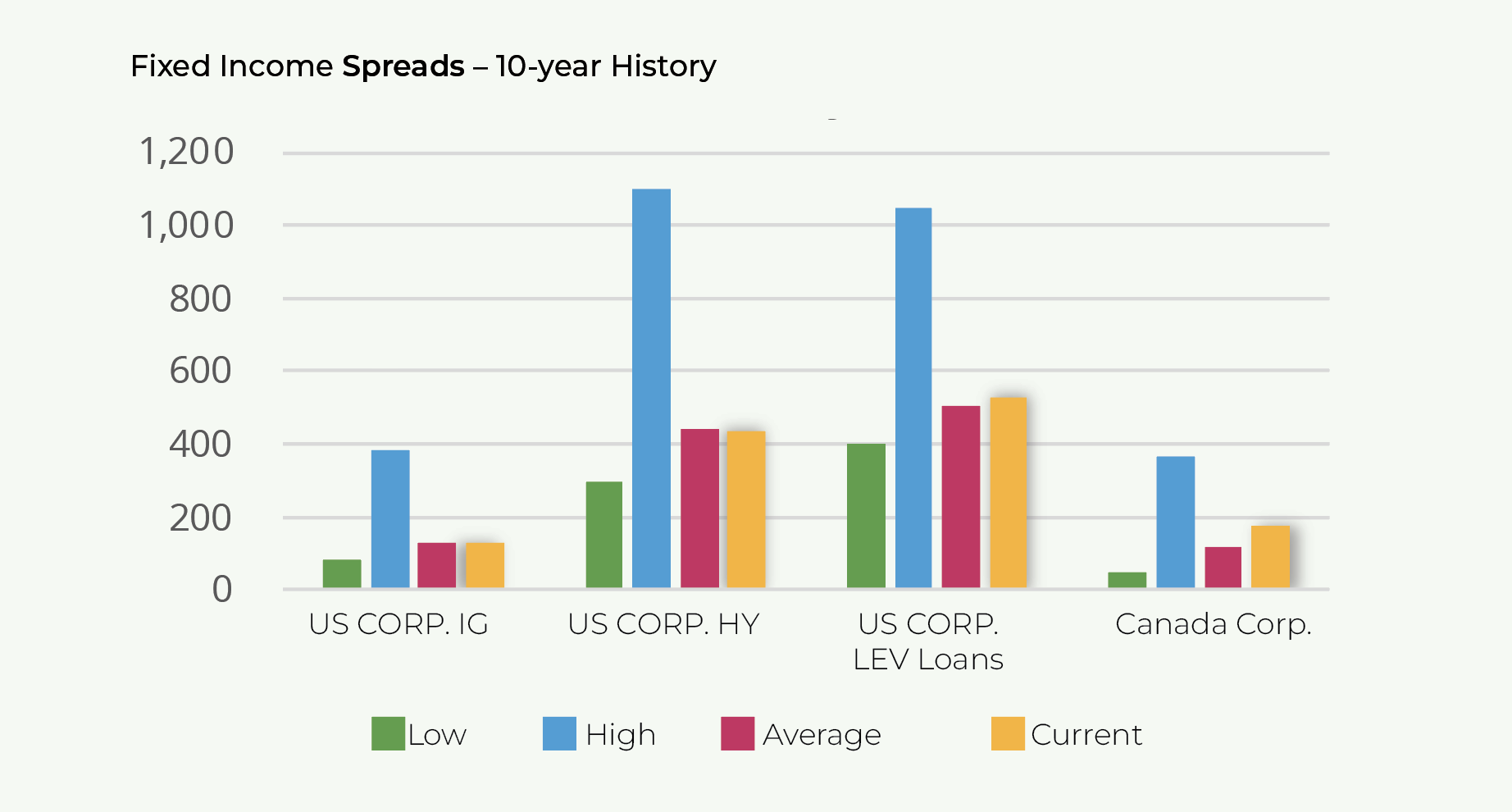

Investment grade corporate bond spreads have modestly declined YTD while high yield bond spreads have tightened more significantly.

IG spreads are presently at 125bps (vs. 141bps at YE 2022) and HY spreads are at 379bps (vs. 469bps at YE 2022).

HY spreads are at the lowest levels since April 2022.

Spreads have generally widened further during prior recessionary periods (200bps for corporate bonds and 800bps for HY bonds).

However, the quality of the high yield index is much stronger now than in previous periods. When coupled with today’s high base rates, it is unlikely that spreads will widen to those experienced in previous recessions (even if economic activity slows substantially).

Signs of credit stress are increasingly emerging with default rates increasing (off very low base levels) and corporate bankruptcy filings reaching levels not seen since the GFC.

Defaults have increased to 2.0% as of Q2 2023 on a trailing twelve-month basis vs 0.8% as of Q2 2022. S&P is forecasting that default rates will increase to 4.0% by YE 2023 and 8.0% by YE 2024. Thus far, S&P has overestimated the pace of increase in default rates. We continue to expect that the default severity will be lower than that experienced during the GFC.